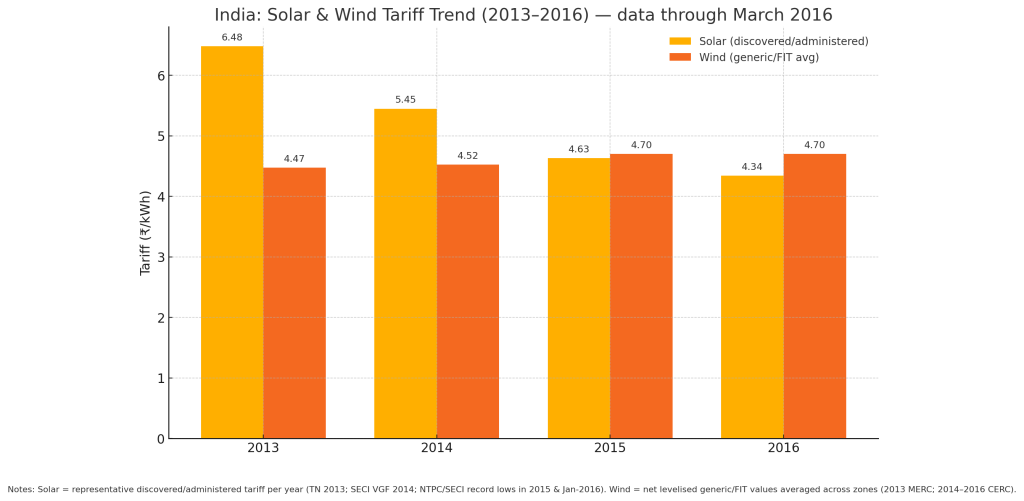

India’s energy story is changing faster than most expected. When the Bhadla Solar Park auction in Rajasthan slipped below the psychological ₹4.34/kWh mark earlier this year, it did more than set a record, it reset expectations. Sunshine can now compete with coal in several regions. This reflects genuine market sentiment, not just industry optimism.

The 175 GW Mandate: A Defining Energy Transition

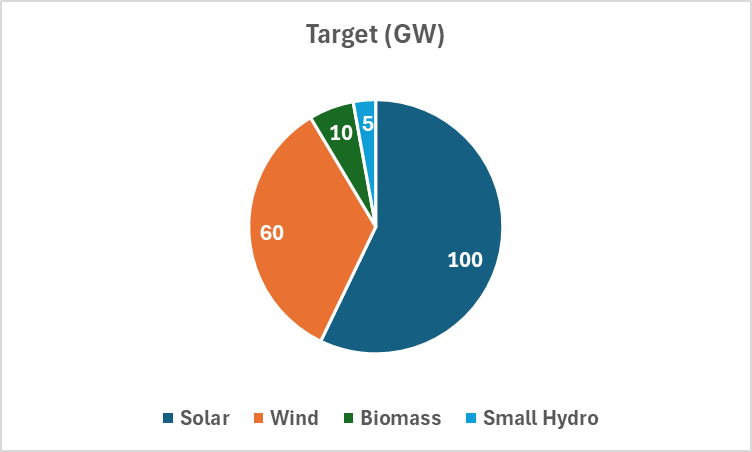

India has committed to install 175 GW of renewable capacity by 2022. It’s venturous by any measure:

100 GW solar, 60 GW wind, 10 GW biomass, 5 GW small hydro. The key drivers to set this goal are Paris commitments, reduction in imported fossil fuel and future energy .

Since the Jawaharlal Nehru National Solar Mission, policy has shifted from modest feed-in tariffs to competitive reverse auctions. Solar parks are taking shape, 34 sites were sanctioned by March 2016-with land and evacuation planned up front. Even so, the arithmetic is stern: as of end-March 2016, India’s renewables stood near 43 GW. Hitting 175 GW means adding >130 GW in six years, or 20+ GW per year, versus ~3 GW added in FY2015–16. The ramp is the story.

What the Price Signal from Bhadla Really Says

The sub-₹4.34/kWh outcome is not an isolated event; it reflects falling module prices, scale in park infrastructure, and better financing. But it also raises the bar. Aggressive bids compress headroom for delays, curtailment, or counterparty risk. This is the fine line for 2016–2018: compete hard, but bank responsibly.

Policy in Mid-2016: Clarity Helps, Whiplash Hurts

The Union Budget 2016 sent mixed signals. On the positive side, the clean energy cess on coal doubled from ₹200 to ₹400/tonne, nudging the market towards lower-carbon choices and channelling funds to clean energy (albeit with uneven on-ground disbursal to date). On the other hand, accelerated depreciation (AD)- particularly important for wind- drops from 80% to 40% from April 2017. For projects modelled on the older incentive, that’s a real dent.

Takeaway for investors: stability often matters more than subsidies. If support will taper, signal it early and stick to the glide path.

The DISCOM Dilemma: Reform or Relapse

Every road leads to state DISCOMs. With debt above ₹3 trillion and payment delays routine in several states, counterparty risk inflates financing costs and erodes developer confidence.

The late-2015 Ujwal DISCOM Assurance Yojana (UDAY) is a two-part answer: state take-over of 75% of DISCOM debt plus performance compacts on losses, metering, and tariff discipline. It is a credible bridge but implementation is the destination. Without genuine reductions in technical/commercial losses and timely tariff revisions, the debt cycle returns, only larger.

Markets Are Maturing: Competitive, Cautious, Creative

Successive auctions compress tariffs; financing must keep up with risk reality

Developers are adjusting. Financing structures are diversifying. We see greater reliance on stronger off-takers (SECI/NTPC), and growing interest in hybrids (solar + wind) to smooth output and improve AC capacity utilisation. Wind is recalibrating to a post-AD world, shifting from tax-led volume to returns-led discipline.

India’s renewables are moving to market-push from the policy pull. The success will depend on the parameters like capital investment, operational cost and efficiency.

Consumers Step Forward: Rooftops and Resilience

Commercial and industrial users are quietly reshaping the grid from the edge. If a plant buys power at ₹6–7/kWh and can self-generate at ₹5–6/kWh, the economics are straightforward. Net-metering policies add further appeal.

For DISCOMs, this is double-edged: high-paying loads self-supply, pressuring revenues. The strategic pivot is to become platform utilities, managing distributed assets and services—rather than defending only kWh sales.

Financing the Build-Out: From Ambition to Allocation

Indicative investment needs to 2022 are ~USD 190 billion. Domestic banks are stretched on power exposure; foreign capital remains wary of off-taker risk and currency risk. The 2016 uptick in green bonds is encouraging, but we also need credit enhancement, currency-hedged vehicles, and robust PPA enforcement to lower the weighted average cost of capital. Execution consistency is the cheapest de-risking tool we have.

Integrating Variable Renewables: The Grid Is the Product

Adding MW is one job while absorbing MWh is another. The Green Energy Corridor, led by Power Grid Corporation India and the states, is the back bone that links demand hubs to the resource-rich zones to demand hubs. To achieve the bold and tough target investments for 2016-2018 should be made as per the below priority Priority:

- Transmission: dedicated corridors and dynamic reactive support.

- Forecasting & scheduling: enforceable, granular, and integrated with SLDC operations.

- Flexibility: storage pilots, demand response, and coal fleet operated for ramping (not just baseload).

Coal PLFs already dip below 60% in places. The planning task is co-optimisation, not cannibalisation.

Key Enablers for Momentum (2016–2018)

- Policy Consistency

Publish a taper schedule where incentives will change; avoid retroactive shocks. Bankability loves predictability. - Deepen DISCOM Reform

UDAY must translate into loss reduction, billing efficiency, and timely tariffs. Link state support to metered milestones, not just MoUs. - Grid Modernisation & Storage

Treat flexibility as infrastructure: storage, peaking capacity, and better data. Fund pilots with a line of sight to scale.

Outlook: From Target to Transformation

India’s renewable journey is about pace and no longer about potential . Technology is competitive. Investor interest is real, and public sentiment has shifted. What remains is the grind of execution: contracts honoured, payments made, grids strengthened, and policies aligned.

If the next few years deliver even half of the planned additions, the structural impact will be immense. A cleaner power mix means lower import bills, improved air quality, and a more resilient economy.

The world is watching, but more importantly, so are India’s own industries and citizens — eager to see whether the promise of affordable, clean power can move from policy papers to the plug points that light up their homes and businesses.