Introduction: India at a Solar Crossroads

India is in the middle of a once-in-a-generation energy transition. For decades, coal has been the backbone of the grid, supported by hydropower and a small share of gas. But now, solar is moving from the margins to the mainstream.

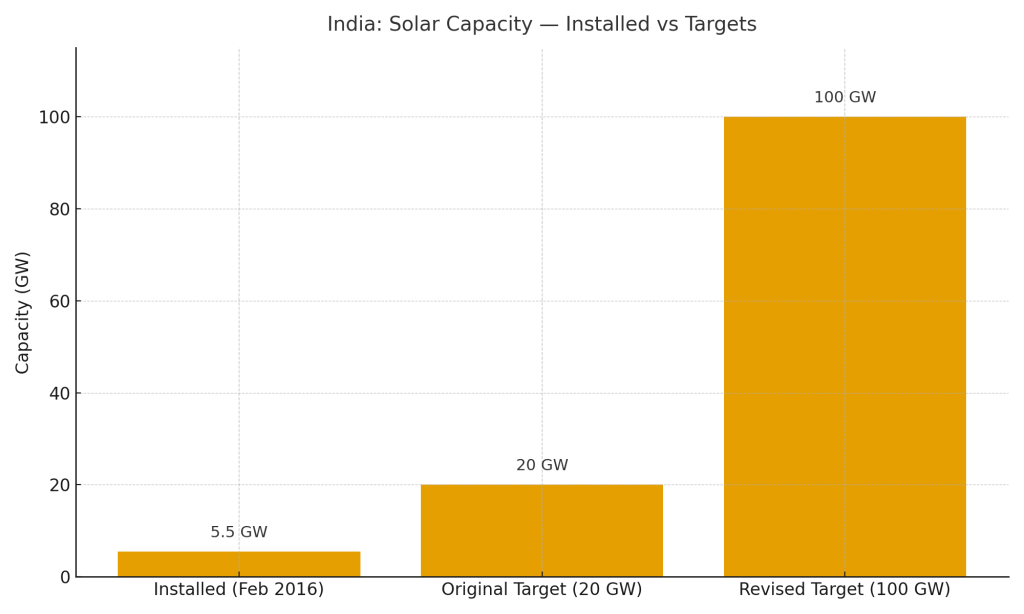

In just a few years, national ambition has scaled dramatically. The National Solar Mission, initially targeting 20 GW by 2022, has been revised to an eye-popping 100 GW. Forty gigawatts are expected from rooftop solar alone - a scale that would have seemed unthinkable just five years ago.

Yet ambition is only half the story. A grid built for predictable baseload coal is now being asked to absorb gigawatts of sunlight - an energy source that arrives when it pleases, sometimes in surges, sometimes in lulls. For policymakers, engineers, and businesses in 2016, this is not a theoretical challenge. It is happening now, and the stakes are enormous: reliability of supply, financial health of utilities, and India’s credibility on the global climate stage.

India’s solar capacity targets (20 GW → 100 GW) alongside actual installed base (~5.5 GW).

A Surge of Solar Power

Policy Meets Market Momentum

India’s solar market has shifted gears. After years of incremental growth, 2015 saw installations jump 142%, breaking through stagnation. As of early 2016, grid-connected solar capacity has crossed 5.5 GW, with expectations for nearly another 4–5 GW this year.

Policy signals are a key driver. The revised targets, combined with programs like solar parks, viability gap funding, and state-level solar policies, have unlocked investor interest. But policy alone does not explain the acceleration.

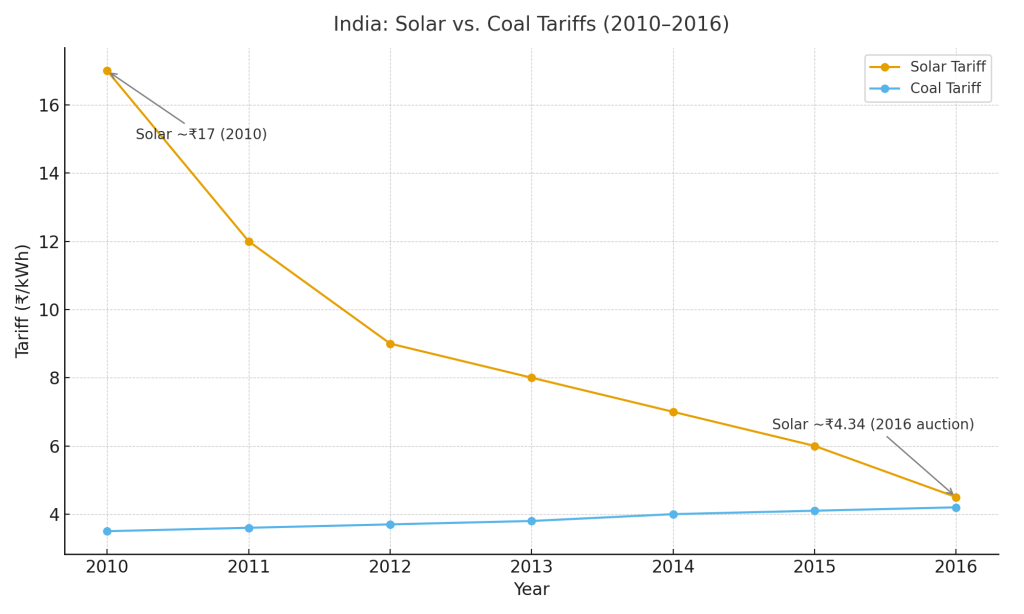

The Price Shock That Changed Everything

In early 2016, the Bhadla solar park auction in Rajasthan sent shockwaves through the sector. Developers bid ₹4.34/kWh, smashing the Central Electricity Regulatory Commission’s benchmark of ₹7.04/kWh for solar PV.

This was not just a cheaper number on paper. It marked a turning point: solar was no longer “expensive green power.” It was now directly competitive with coal in certain contexts. Developers, lenders, and consumers all took notice.

Falling module prices, global oversupply (particularly from China), and intense competition combined to create a new cost reality. Suddenly, the 100 GW target did not feel like fantasy.

Solar tariffs in India (2010–2016) vs. coal tariffs

The Grid’s Growing Pains

The success of solar deployment brings with it a complex set of challenges. These challenges are technical, institutional, and financial - and they are all intertwined.

1. The Variability Challenge

Solar is predictable on average but volatile in the moment. A passing cloud can cause sharp drops in output. Evening peak demand arrives just as solar disappears. For engineers, this is not just inconvenient - it threatens the delicate balance of frequency (50 Hz) and voltage that keeps the grid stable.

India’s coal plants, designed for steady baseload operation, are not naturally suited to rapid ramping. Hydropower offers some flexibility, but seasonal dependence limits its availability. Without flexibility, grid operators face an uphill battle.

2. Transmission Bottlenecks

The mismatch between where solar is generated and where it is consumed is a serious hurdle. Rajasthan and Gujarat boast some of the highest solar potential in the world. Yet the demand centers are hundreds of kilometers away in cities like Mumbai, Delhi, and Bangalore.

Transmission expansion is underway, but not at the pace solar deployment demands. The result is congestion - and, in some states, forced curtailment of solar output. Developers, already operating on tight margins, see curtailment as a financial risk.

3. The DISCOM Dilemma

Distribution companies (DISCOMs), the financial backbone of the sector, are under enormous stress. Saddled with debts, reliant on cross-subsidies, and often behind on payments, they view solar as both opportunity and threat.

Large consumers - industries and commercial buildings - are turning to rooftop solar to cut their bills. For DISCOMs, this erodes the very revenue streams that cross-subsidize household and agricultural supply. As a result, many DISCOMs hesitate to sign new power purchase agreements (PPAs) with solar developers, slowing integration.

Emerging Solutions: Building Flexibility

Despite the hurdles, solutions are already being tested across India. The transition will not be easy, but early steps are promising.

Energy Storage: The Safety Net

Lithium-ion battery prices have fallen more than 70% since 2010, making storage a serious option for the first time. In India, SECI’s solar-plus-storage tenders are breaking new ground. While still small in scale, these pilots will generate crucial insights on cost, performance, and operational integration.

Image Placeholder:

Diagram showing solar PV feeding both grid and battery storage.

Suggested Caption: Storage captures excess solar and releases it during peak demand.

Smart Grids: Intelligence at the Edge

The National Smart Grid Mission (NSGM), launched last year, is the institutional push toward a modernized grid. Smart meters, demand-side management, microgrids, and real-time monitoring are all part of its agenda.

A smarter grid means two-way flows of power, better visibility for operators, and smoother integration of distributed generation like rooftop solar.

Flexible Conventional Plants

Coal and gas plants, far from being obsolete overnight, can be part of the solution. By retrofitting plants to operate more flexibly, they can provide the ramping support needed to stabilize solar’s fluctuations. While not the cleanest option, it offers a pragmatic bridge until storage and demand response scale up.

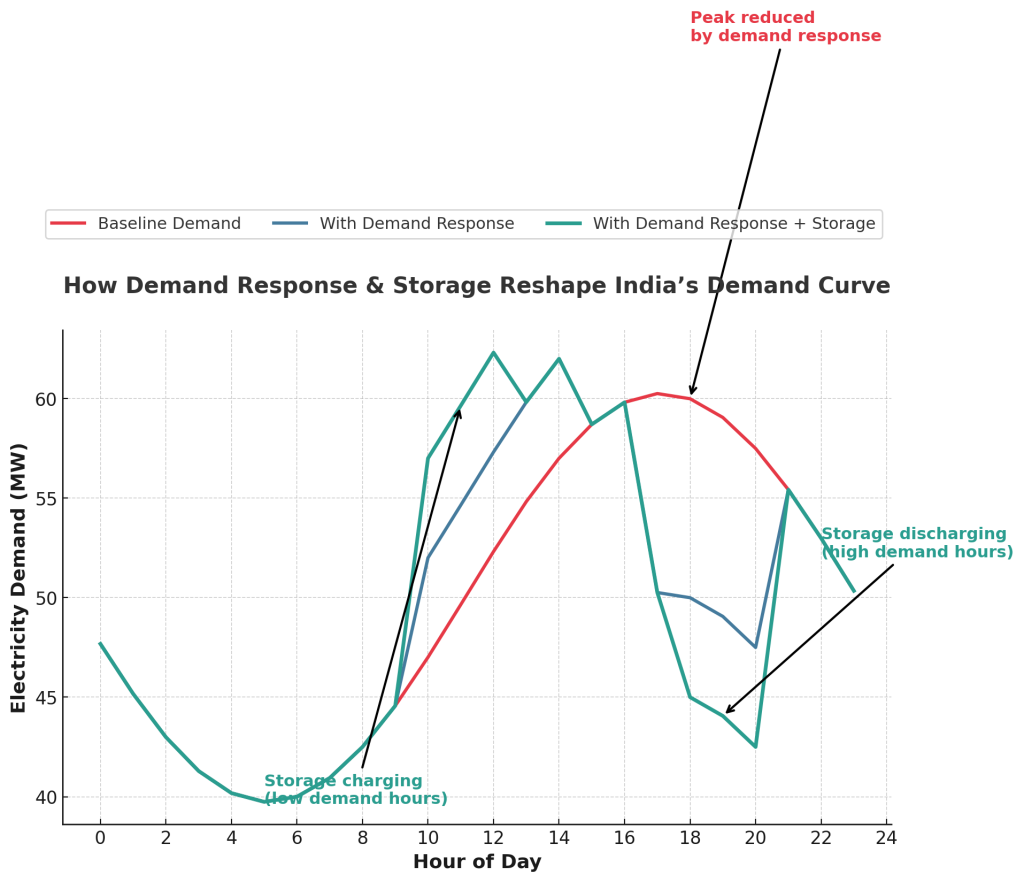

Demand Response: Shaping the Load Curve

Shifting demand to match supply is a radical but necessary shift. Instead of always meeting demand instantly, India can encourage consumers to adapt their usage patterns.

Time-of-use tariffs are a practical lever: cheaper power during sunny hours, higher rates during peaks. Early adopters - from data centers to textile mills - could become champions of this new flexibility.

Smarter demand can make variable solar easier to integrate

Learning from India’s Pilots and Global Peers

India’s Trailblazers

Projects like Bhadla Solar Park and SECI’s storage pilots are more than headlines. They are test beds for the future. Each auction, each tender provides insights into cost, risk allocation, and technical feasibility.

Lessons from Germany

Germany’s Energiewende demonstrates both ambition and risk. Rapid renewable growth has destabilized the business models of traditional utilities, leaving stranded assets and financial losses. For India, with its fragile DISCOMs, the lesson is urgent: integration must be managed carefully, or the system could collapse under its own contradictions.

Lessons from Japan

Japan proves that technical challenges can be overcome. Despite its fragmented grid and lack of international interconnections, it has successfully integrated high shares of solar. For India, this is an encouraging sign that scale is not a barrier - provided grid practices are robust.

Policy Levers and Actionable Insights

Policy is the invisible hand guiding India’s solar transition. The National Tariff Policy (2016) is a pivotal piece:

- Mandatory Solar Procurement: DISCOMs must procure at least 8% of consumption from solar by 2022.

- Transmission Incentives: Solar and wind projects enjoy waived inter-state charges, making cross-country flows viable.

- Competitive Bidding: Moves procurement firmly toward auctions, locking in efficiency and cost reductions.

But deeper reforms are essential. The UDAY scheme has begun addressing DISCOM debts, yet structural issues remain. Without financially healthy utilities, even the cheapest solar will struggle to find buyers.

Transmission investments must accelerate. Smart grids need scale, not pilots. And consumer-facing policies - especially around demand response and rooftop solar - must be pushed harder to unlock flexibility.

Conclusion: A Look Ahead

India’s solar revolution is real, and it is already reshaping the energy sector. Costs have plummeted, projects are scaling, and global attention is fixed on whether the world’s fastest-growing economy can also become a renewable leader.

But success is not guaranteed. Integration challenges, if left unaddressed, could stall progress. Transmission build-out, DISCOM reforms, smart grid rollouts, and demand-side innovation must all keep pace.

For engineers and professionals working in the sector, this is a defining moment. The solutions tested today - from flexible coal retrofits to pilot storage projects - will form the blueprint for the next decade.

The grid of the future will not look like the grid of the past. It will be smarter, more flexible, more interactive, and more decentralized. The question is not whether solar will rise - it already has. The question is whether the grid can rise with it.