A New Dawn for India’s Energy Transition

India’s energy landscape is entering a transformative era. The National Green Hydrogen Mission (NGHM) has moved beyond policy discussions to become a real catalyst reshaping the power sector. The early results from the Strategic Interventions for Green Hydrogen Transition (SIGHT) auctions and other pilot initiatives demonstrate that hydrogen is no longer a futuristic concept but an actionable lever for national energy strategy.

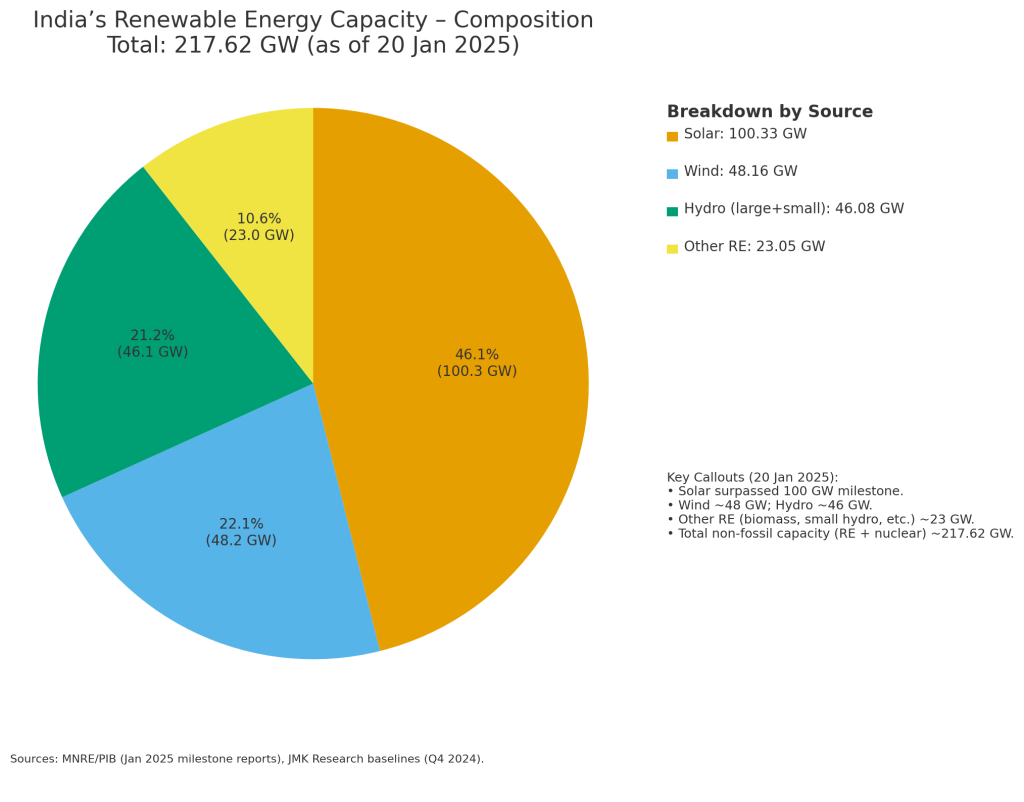

The country’s renewable energy momentum is impressive: over 24 GW of solar and 3 GW of wind capacity were added recently, bringing non-fossil fuel capacity to more than 217 GW. The NGHM leverages this renewable potential to achieve strategic energy goals, including long-term energy independence and a net-zero economy trajectory.

The Blueprint for a New Energy Economy

The NGHM is designed to make India a global hub for green hydrogen production and export, including derivatives like green ammonia and green methanol. It aligns closely with Aatmanirbharta (self-reliance), aiming to reduce fossil fuel imports, which stood at $190 billion in 2024, and to save approximately ₹1 lakh crore by 2030.

SIGHT Program: Driving Production and Manufacturing

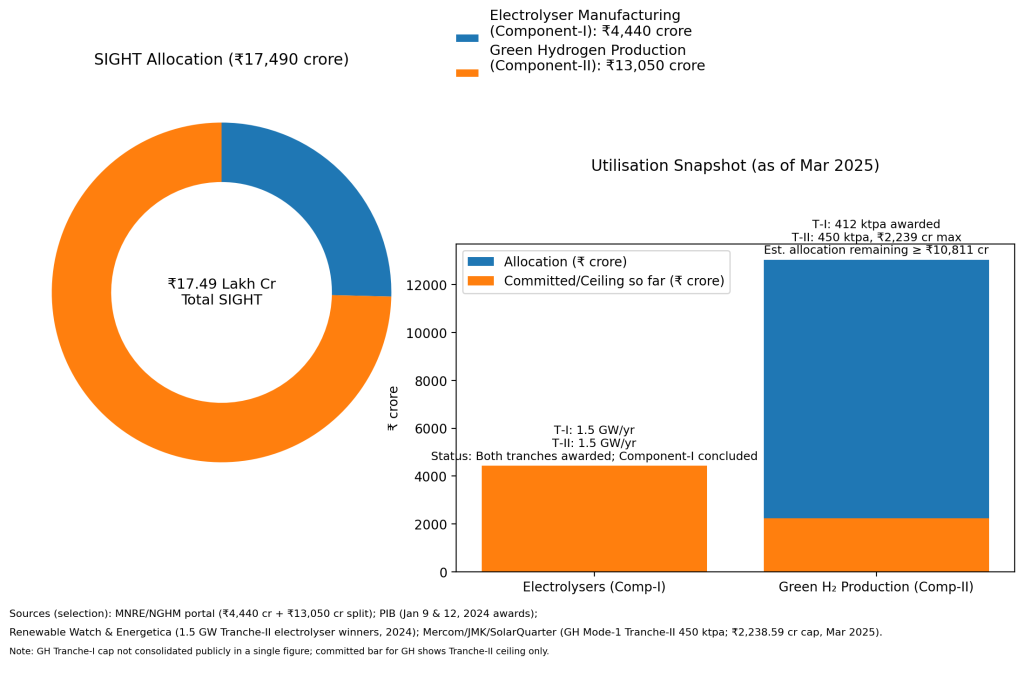

The SIGHT program, with an initial allocation of ₹17,490 crore, provides targeted support for:

- Domestic electrolyzer manufacturing

- Green hydrogen production

This dual approach is designed to lower production costs, create a robust supply chain, and accelerate industrial adoption. By integrating both upstream and downstream incentives, India seeks to build self-sufficiency and competitiveness in this emerging sector.

Globally, green hydrogen has faced hurdles due to high costs and regulatory uncertainty. India’s policy-driven, auction-based approach provides a more de-risked path for private investment, distinguishing it from countries where projects have been delayed or cancelled.

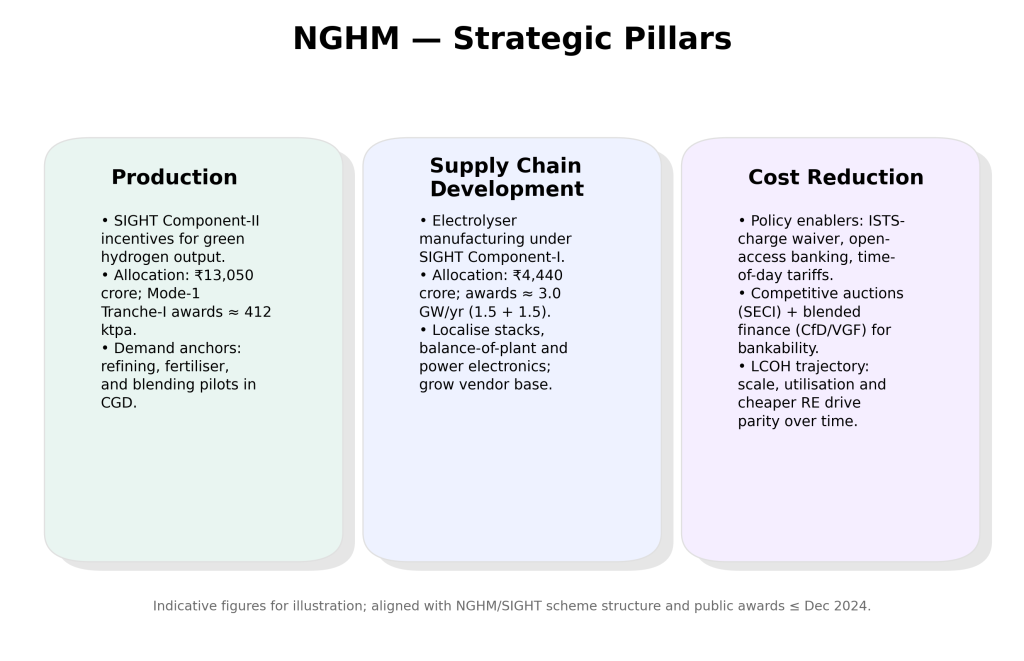

NGHM’s strategic pillars: production, supply chain development, and cost reduction

Implications for Key Stakeholders

The DISCOM Equation: From Challenges to Strategic Assets

Achieving 5 MMTPA of green hydrogen production will require:

- 135 GW of renewable energy capacity

- 74 GW of electrolyzer load

This influx of intermittent power demands quadrupled grid flexibility, from ~250 MW/min to ~1,100 MW/min during peak hours.

For DISCOMs, high-paying industrial consumers may shift to captive generation or open access, impacting revenues. However, electrolyzers can serve as smart grid assets, absorbing excess renewable energy during peak production and reducing demand when the grid is stressed. This capability also mitigates renewable curtailment and decreases reliance on expensive battery energy storage systems (BESS).

Practical Example: Grid Management in Action

States like Maharashtra and Gujarat, with abundant solar and wind resources, are already piloting hydrogen electrolyzers to balance peak renewable output. By coordinating grid dispatch with electrolyzer operations, these regions demonstrate reduced curtailment, improved load management, and potential cost savings for DISCOMs.

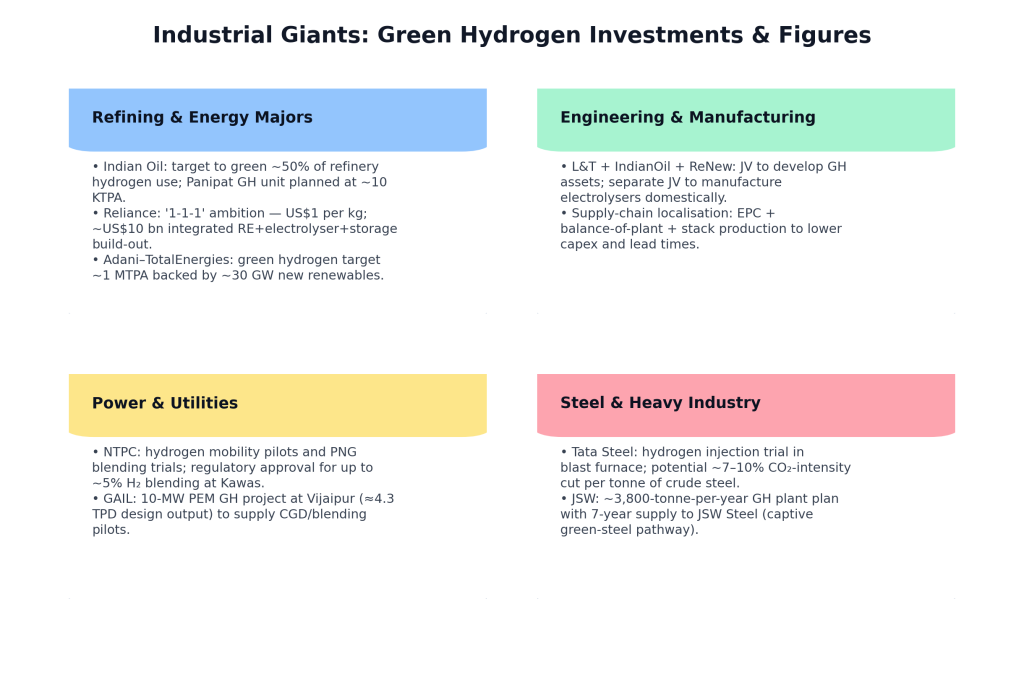

Industry Leaders: Green Hydrogen as a Competitive Advantage

Green hydrogen adoption is driving strategic investments across hard-to-abate sectors such as fertilizer, steel, and refining. Major corporations like Reliance Industries, L&T, and Indian Oil are building integrated clean energy ecosystems rather than treating hydrogen as a compliance measure.

Examples:

- Indian Oil: Plans to convert 50% of its hydrogen use to green hydrogen by 2030, supported by a ₹2.5 lakh crore investment.

- Reliance Industries: Developing a 30 GWh battery giga-factory alongside electrolyzer facilities, integrating production with storage solutions.

Green hydrogen positions India’s industries to remain globally competitive as carbon regulations tighten. Companies investing early gain cost advantages, brand recognition in sustainability, and preparedness for stricter international standards.

Industrial giants investing in green hydrogen to decarbonize operations and gain a competitive

Indian Oil (IOCL): target to green ~50% of refinery H₂; ~10 KTPA Panipat green-hydrogen unit planned.

Reliance: “1-1-1” ambition (US$1/kg); ~US$10 bn integrated green-energy ecosystem.

Adani–Total Energies: ~1 MTPA green H₂ target backed by ~30 GW new renewables.

L&T + IOCL + ReNew (JVs): asset-development JV + electrolyser-manufacturing JV to localise supply chain.

NTPC: hydrogen mobility/blending pilots; PNGRB approval for ~5% H₂ blending at Kawas PNG network.

GAIL: 10 MW PEM project at Vijaipur (design output ~4.3 TPD).

Tata Steel: blast-furnace H₂ injection trial; potential ~7–10% CO₂-intensity cut per tonne of crude steel.

JSW (Energy/Steel): plan for ~3,800 t/yr green H₂ with a 7-year supply arrangement for JSW Steel.

Consumers: Economic and Future Mobility Benefits

For individual consumers, the benefits are primarily macro-economic in the near term:

- 6 lakh jobs projected by 2030

- ₹1 lakh crore reduction in fossil fuel imports

In the medium term, hydrogen applications in transport and mobility will become tangible. Pilot projects for hydrogen-powered trains and planned electric trucks under the PM e-DRIVE scheme hint at a future where hydrogen fuels cleaner, more efficient mobility solutions.

Hydrogen mobility applications are emerging in public transport and freight

Opportunities and Persistent Challenges

Opportunities: India as a Global Hydrogen Hub

India’s solar and wind endowment allows for a potentially low-cost Levelized Cost of Hydrogen (LCOH). The SIGHT program, coupled with a 100% FDI automatic route, is expected to attract over ₹8 lakh crore in investment by 2030.

Clustered investments in industrial hubs and renewable resource-rich regions help:

- Minimize logistics costs

- Accelerate economies of scale

- Foster local manufacturing ecosystems for electrolyzers and fuel cells

Challenges: Cost and Infrastructure

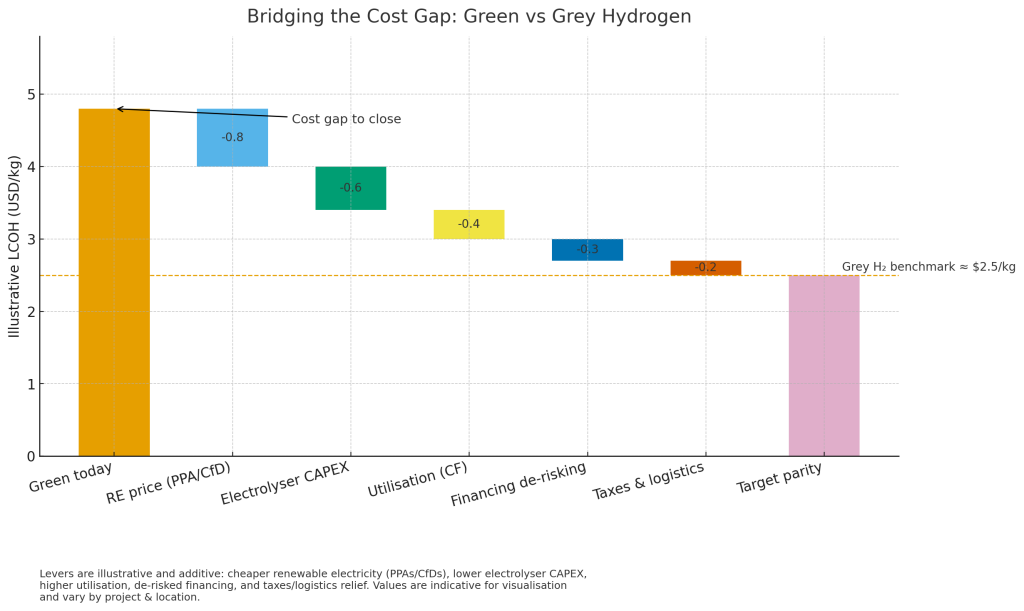

1. Cost Gap

- Green hydrogen: $4–5/kg

- Grey hydrogen: $2.5/kg

High costs arise from electrolyzer CAPEX and renewable energy integration. Bridging this gap is essential for scaling adoption.

2. Infrastructure

- Limited pipelines, storage, and refueling networks

- Logistical and distribution challenges raise delivery costs

3. Regulatory Complexity

- Policies vary across states

- Need for consistent, long-term signals to de-risk private investment

Caption: Reducing the cost gap between green and grey hydrogen is crucial for scaling adoption

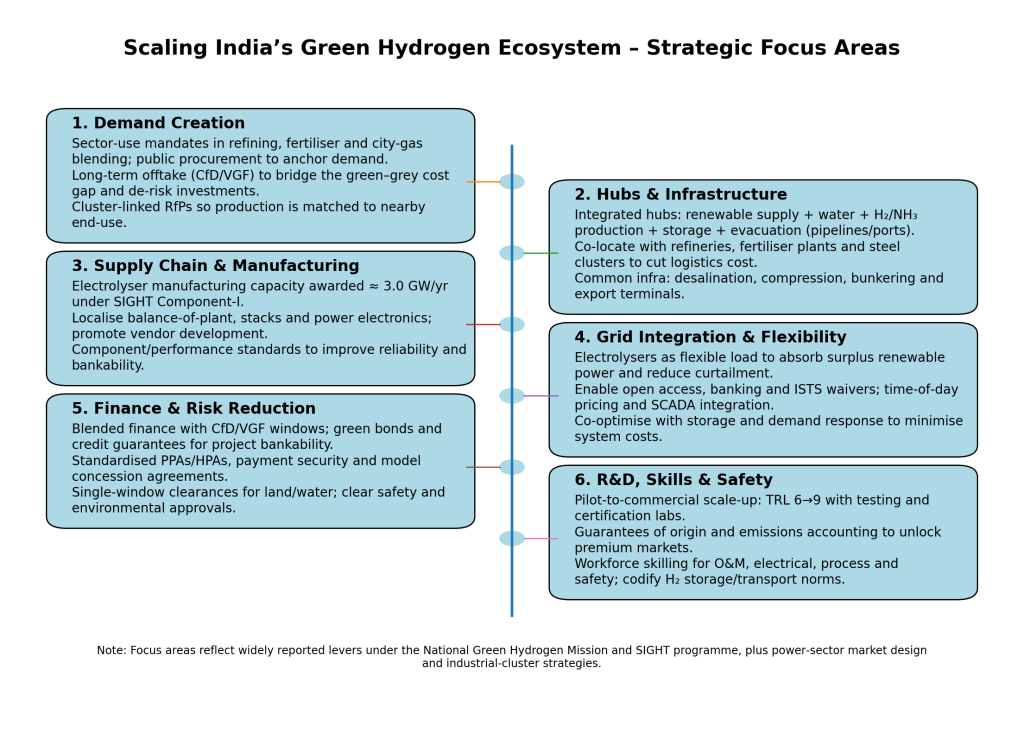

Strategic Priorities for 2025

- Demand Creation: Enforce minimum consumption mandates and leverage public procurement to provide predictable demand for private investors.

- Cluster, Connect, Conquer: Develop integrated green hydrogen hubs in resource-rich regions to optimize supply chains and reduce production costs.

- R&D and Innovation: Transition from academic research to rapid commercialization via testing facilities, pilot projects, and incubation programs.

- Global Collaboration: Harmonize standards, secure technology transfer, and open export markets through strategic international partnerships.

Key priorities for scaling India’s hydrogen ecosystem: demand creation, hubs, R&D, and global alliances.

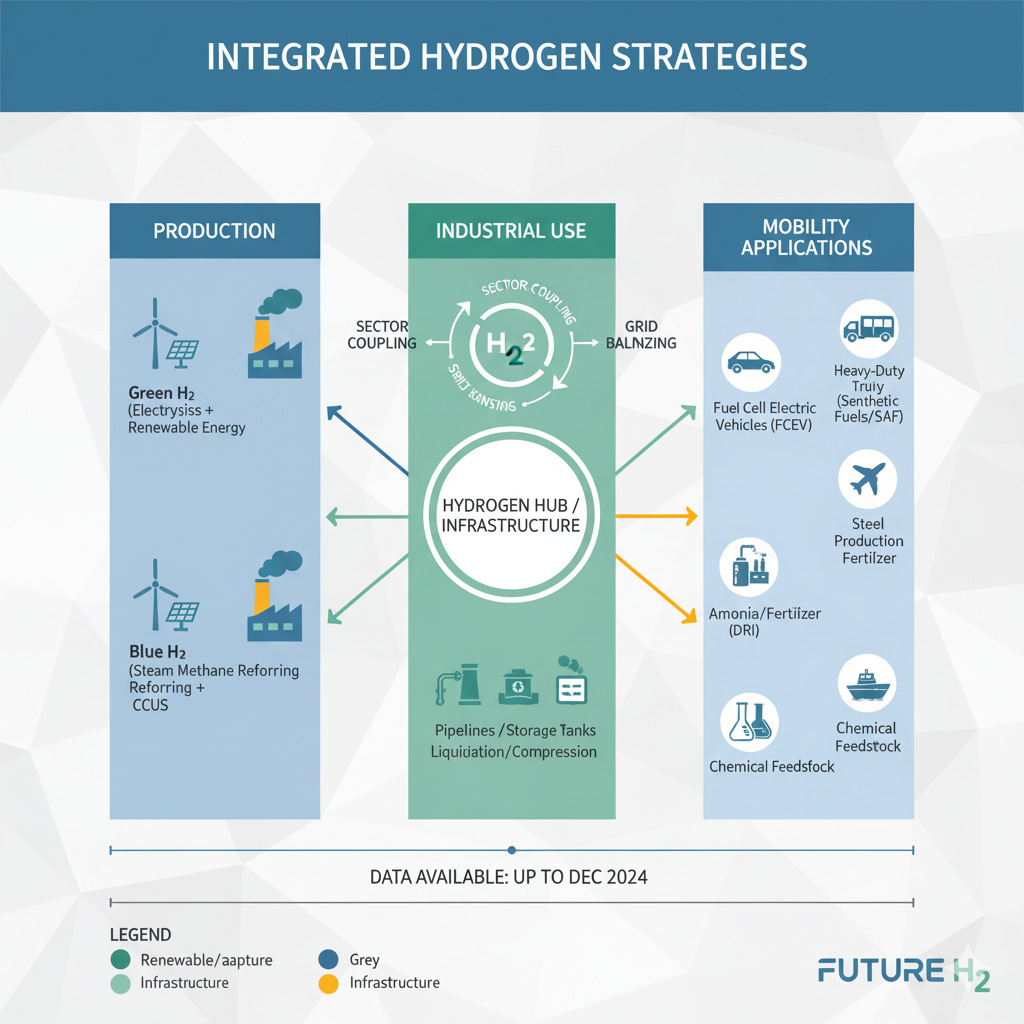

Looking Ahead: Policy, Industry, and Consumer Integration

The NGHM represents a systemic shift for India’s energy, industrial, and mobility sectors. Success depends on aligning:

- Policy incentives with private investment

- Grid management strategies with electrolyzer deployment

- Industrial adoption with consumer mobility applications

States that adopt holistic hydrogen strategies - integrating production, storage, and industrial use - will likely become national exemplars, demonstrating efficiency, economic impact, and export readiness.

Integrated hydrogen strategies link production, industrial use, and mobility applications.

Conclusion: From Strategic Vision to Action

The National Green Hydrogen Mission is more than policy; it is a strategic pivot for India’s energy and industrial future. While challenges remain - particularly cost parity and infrastructure - policy clarity, private sector engagement, and proactive investment provide a roadmap for success.

By focusing on:

- Creating guaranteed demand

- Building integrated hydrogen hubs

- Investing in R&D and innovation

- Forming global alliances

India can not only decarbonize its power sector but emerge as a global leader in green hydrogen, turning energy challenges into economic and strategic opportunities.

Love seeing data on energy conservation. 💚

Thank you for your perspective! Really appreciate your kind words 🔍

This is exactly what sustainability teams need Neeraj

Thank you for reading!

Excellent resource for climate compliance Neeraj!

Appreciate it Arjun!

Really valuable for carbon disclosure

Excellent breakdown of carbon metrics!

Thanks Simran! 💚

Really useful for sustainability KPIs

Fantastic information on clean energy adoption! ⚡

Really appreciate this focus on decarbonization. 💚

Extremely thoughtful Nikhil!

Great insights on green energy solutions Neeraj!

Appreciate it! Very useful 📱

Love this Neeraj, seeing this focus on carbon transparency

Great analysis of renewable capacity Neeraj!

Extremely valuable! Very valuable

This is exactly what we need for ESG excellence!

Great insights on climate accountability Neeraj! 🎯

Appreciate your kind words! Great to hear

This helps with renewable energy planning. 🔋

Appreciate your input! Much appreciated