A New Chapter in India’s Renewable Story

If you have passed through the wind and solar regions of India you will find a new scenario: installation of solar panels and wind turbines side by side. In places like Rajasthan’s open plains and the dry parts of southern India, the view is no longer “solar or wind.” It’s becoming both. At first, this might look like a developer trying to use land more efficiently. But it also shows a bigger change in thinking. India is starting to focus less on adding megawatts and more on what happens after those megawatts come online , how they perform on a real grid, with real limits, and with electricity demand that doesn’t wait for sun or wind.

India’s headline ambition is well known: 175 GW of renewable energy by 2022, including 100 GW of solar and 60 GW of wind. But as the Ministry of New & Renewable Energy (MNRE) itself notes, by the end of FY 2017–18 the country already had nearly 70 GW of installed renewable power capacity. The harder part isn’t announcing targets , it’s making sure the system can absorb what’s being built.

Which leads to a more practical question that grid operators, discoms, and developers have been wrestling with: How do you add large volumes of variable power without turning grid management into daily firefighting?

Why integration matters more than addition

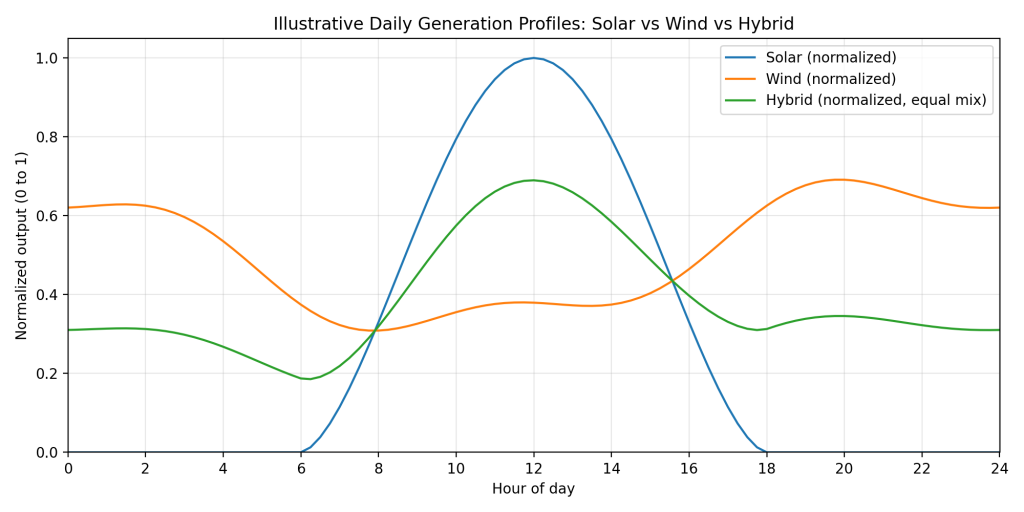

The challenge with renewables isn’t that they don’t generate enough energy. It’s that they don’t generate it when the grid wants it, in the smooth way legacy power systems were designed around.

There’s also a second-order issue that doesn’t get as much public attention: flexibility on the conventional side. Coal plants can ramp, but not infinitely fast and not always cheaply. And grid operation in India , still heavily state-by-state in practice , doesn’t always make it easy to balance variability smoothly across regions.

Large modelling exercises around integrating the 2022 renewables target have pointed out that the system can handle high renewables, but it needs the right operational choices and sufficient transmission. In other words: India’s renewable story is no longer only about building projects. It’s about building a system.That’s where hybrids fit.

The hybrid idea: letting the resource mix do some of the balancing

A solar–wind hybrid, in the simplest sense, is a plant that combines wind turbines and solar PV in a coordinated way , either co-located or tied to the same point of grid connection. MNRE’s newly released policy defines hybrid systems around exactly that: wind and solar configured to operate at the same grid connection point, using one of several possible integration approaches.

There’s also a practical policy definition that matters for developers: under MNRE’s framework, a plant is recognized as “hybrid” if the rated capacity of one resource is at least 25% of the rated capacity of the other.

That 25% threshold isn’t just bureaucracy , it’s meant to ensure hybrids aren’t token add-ons. The objective is to create a generation profile that is meaningfully less jagged than a single-resource plant.

MNRE’s policy puts the logic plainly: studies show wind and solar resources in India often complement one another, and hybridization can reduce variability while also using land and transmission more efficiently. The attractive part is that it’s not a new technology. It’s mostly smart design: use the sun when it’s strong, the wind when it’s available, and push both through shared infrastructure.

Shared infrastructure: the unglamorous win that actually moves the needle

The less poetic (and more bankable) argument for hybrids is this: the most expensive headaches in renewables aren’t panels and turbines anymore. They’re land, right-of-way, and evacuation.

Once a substation and transmission link are built, the question becomes: How fully are you using them?

A standalone solar plant might lean heavily on its evacuation capacity during the middle of the day and leave it underused the rest of the time. Wind might do the reverse. A hybrid can “fill in” those gaps. That’s the kind of system value Discoms and grid operators tend to appreciate because it isn’t only about energy produced, it’s about energy delivered without causing chaos.

MNRE explicitly encourages this logic, including hybridizing existing projects where feasible (adding solar near wind farms, or wind near solar parks), so that existing connectivity and infrastructure can be better utilized.

A real example already on the ground: Hero’s Karnataka hybrid

This isn’t only theory anymore. In April 2018, Hero Future Energies completed what it described as India’s first large-scale solar–wind hybrid project in Karnataka, at Kavithal in Raichur district: an existing 50 MW wind farm paired with a neighbouring 28.8 MW solar PV plant ,while keeping the evacuation capacity at 50 MW.

That last detail is the point. The project wasn’t designed to export a much bigger peak. It was designed to make the existing grid interface work harder, more hours of the day.

And the performance numbers are exactly why hybrids have started showing up in policy conversations. In that project’s case, the reported plant load factors were about 28% for wind and 18.7% for solar, but 41.8% combined for the hybrid system.

That combined PLF doesn’t magically eliminate variability—but it does reshape it into something grid planners can handle more easily. It also makes the financial story cleaner: more consistent output improves the predictability that lenders and long-term offtakers tend to reward.

Policy is catching up

For years, hybrids sat in an awkward gap. Everyone agreed the concept made sense, but the rules weren’t clear: tariff treatment, scheduling, metering, and how to count hybrid power toward different RPO buckets.

That’s why MNRE’s move this May matters.

On 14 May 2018, MNRE released the National Wind–Solar Hybrid Policy, explicitly framing hybrids as a grid-oriented solution: better utilization of land and transmission infrastructure, reduced variability in renewable generation, and improved grid stability.

The policy also does something important in the Indian context: it tries to bring hybrids out of the “special pilot” category and into the mainstream toolbox , covering new plants, hybridization of existing assets, and the role of storage.

On storage, MNRE is careful but clear: battery storage may be added to reduce variability, increase delivered energy for a given sanctioned capacity at the delivery point, and even support “firm power” for specific hours.

It also flags a key implementation reality: until standards and regulations for DC metering and related issues are in place, only AC integration would be permitted. This is the kind of detail that tells you the policy was written by people who have dealt with real grid and metering questions, not just PowerPoint ambitions.

And notably, the policy calls for CEA and CERC to formulate standards and regulations around metering methodology, forecasting and scheduling, connectivity, and other requirements for hybrid systems. This is exactly where the “hybrid era” will either accelerate or stall.

Procurement is already lining up behind the idea

Even without waiting years for perfect regulatory clarity, the procurement pipeline is beginning to point toward hybrids.

By the end of May, reporting around India’s planned hybrid tenders suggested the government had sanctioned a 2.5 GW tendering scheme for hybrid wind–solar capacity, with SECI appointed as the nodal agency and with an explicit allowance for developers to install “any energy storage facility” alongside projects if they choose.

That last clause is telling. It signals that policymakers aren’t treating storage as a separate, niche experiment. They’re starting to see it as a layer that can sit on top of hybrid generation when the economics make sense.

At the same time, not everyone is convinced hybrids are the cheapest route to grid stability. Commentary around the May 2018 tender plan included the view that forecasting improvements, ancillary services, and demand-side management may sometimes deliver similar stability benefits at lower cost. That scepticism is healthy and it’s part of why 2018 feels like a real turning point: hybrids are moving from “concept” to “market test.”

Storage: the next layer, but still expensive in 2018

If hybrids are the near-term “integration move,” storage is the long-term one. But in 2018, batteries are still hard to justify at scale on pure cost terms for grid-tied renewables.

Early 2018 reporting around storage economics (based on industry conference discussions and modelling) pegged lithium-ion battery pricing at around US$350/kWh in at least one referenced set of assumptions for grid-integration scenarios.

That doesn’t mean storage is irrelevant. It means storage is likely to show up first in places where it earns revenue beyond energy shifting: fast response, ancillary services, local congestion relief, and firming for specific contracted hours.

MNRE’s hybrid policy, notably, already anticipates that arc , recognizing storage as an add-on that can reduce variability and support firm output requirements when procurement designs call for it.

What hybrids really represent in 2018: a mindset change

It’s tempting to treat solar–wind hybrids as just the next project type, like floating solar or higher hub-height turbines. But hybrids are different, because the value proposition is not only about generation , it’s about behaving well on the grid.

That’s a subtle but important change in India’s renewable narrative.

Until recently, success was mostly counted in gigawatts commissioned. Now, there’s growing pressure to prove that renewable plants can be planned as system resources , predictable enough, stable enough, and economically sensible enough for large-scale integration.

The MNRE policy itself reflects that shift, framing hybrids around optimal infrastructure use and reduced variability rather than only capacity addition. And the early projects , like the Karnataka hybrid example—show how developers are already using hybrids to raise combined plant load factors and make better use of limited evacuation capacity.

Looking ahead, from June 2018

From where we stand now, hybrids look less like an experiment and more like an inevitable next step , especially in states where land and transmission are already contested.

Three things will decide how fast hybrids scale:

1) Tariff discovery that buyers can trust.

Hybrids need procurement structures that reward the value they provide—whether through better CUF/PLF, firmer delivery windows, or reduced variability.

2) Real operational rules (not just policy intent).

Scheduling, forecasting, metering, and deviation settlement are where projects either become “grid-friendly” or become another source of friction. MNRE has already pushed the baton toward CEA and CERC for this part.

3) Storage economics that stop being hypothetical.

Batteries will get cheaper over time, but in 2018 they are still expensive enough that hybrids will likely carry the early integration burden largely on their own.

If these pieces align, India won’t just be renewable-rich but it will start becoming renewable-reliable. And that distinction is what will matter most when renewables stop being the “new” part of the mix and become the backbone.