I. A Judicial Push That Changes Everything

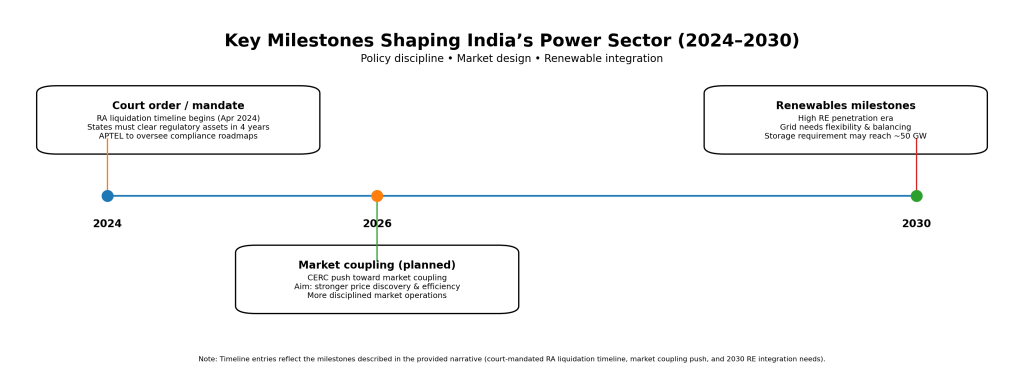

In August 2025, India’s Supreme Court delivered a landmark verdict that could define the next two decades of the power sector. As per the directive of Supreme Court, all states must liquidate regulatory assets (RAs) within four years, starting April 2024.

For years, these deferred debts that are essentially unpaid dues parked on distribution companies’ balance sheets have been quietly accumulated. By 2025, just seven states held nearly ₹3 trillion in such assets. DISCOMs, already saddled with losses, treated these as temporary, but they snowballed into a systemic problem.

The court cut through decades of political hesitancy. Unlike earlier reform schemes, which often met resistance at the state level, this mandate isn’t optional. The Appellate Tribunal for Electricity (APTEL) will oversee compliance, forcing states to create concrete recovery roadmaps, through tariff reforms, subsidy transparency, and better financial governance.

This is not just a policy shift. It’s a judicial shockwave that changes the balance of power in the electricity sector. For the first time, states cannot defer the problem but they must face it.

II. DISCOMs at a Crossroads

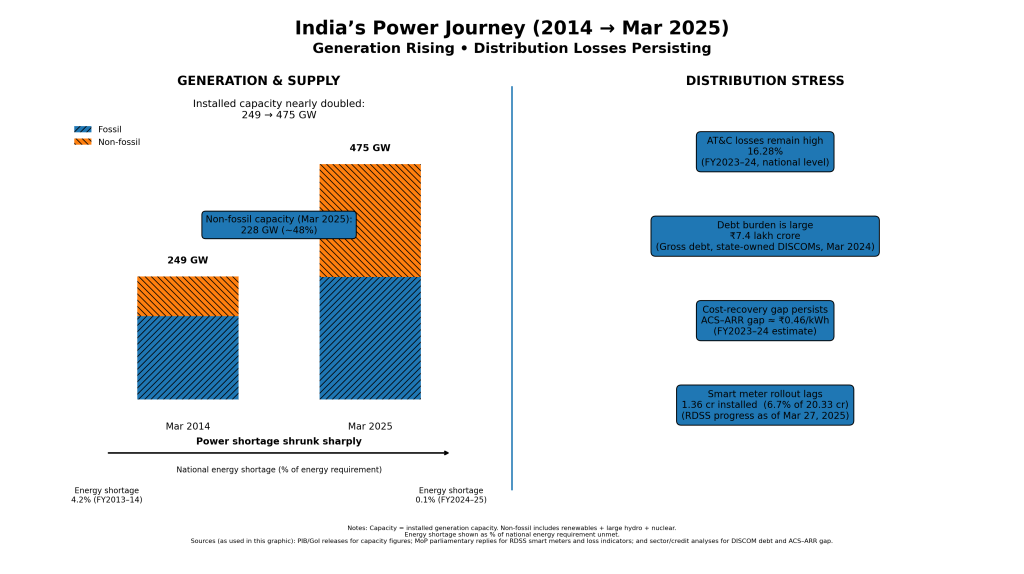

On paper, India’s power sector looks impressive. Installed capacity reached 476 GW by June 2025, with almost half of it from non-fossil sources. Power shortages, once a daily headline, are now negligible.

But scratch below the surface, and the distribution segment tells a different story:

- ₹7.4 lakh crore debt piled up by March 2024.

- ACS-ARR gap of 46 paise/unit in FY24 : revenues still falling short of costs.

- Median tariff hike of just 1.9% for FY26 : well below the 4.5% needed.

- 51 out of 70 DISCOMs running losses.

- Smart meters lagging badly: ~20 million installed, vs. 250 million target.

This financial shakiness sets off a nasty chain reaction: DISCOMs get cold feet on new renewable PPAs, investors bail out, and state subsidies just keep ballooning out of control

India has made its mark in power generation, but the real challenge now lies in distribution.

India’s paradox: generation success vs. distribution stress

III. The Three Forces That Will Shape 2040

Looking ahead, India's power distribution sector will be driven by three big forces coming together: solid policy discipline, digital breakthroughs, and more private players jumping in.

1. Policy & Regulatory Discipline

The Supreme Court ruling is the most decisive regulatory moment in years. Cost-reflective tariffs can no longer be avoided. Combined with new rules , such as legal clarity on storage assets and the Central Electricity Regulatory Commission’s (CERC) push for market coupling by 2026, we’re moving toward a more disciplined, transparent sector.

If enforced properly, these rules could unlock a culture of accountability that decades of reform programs struggled to deliver.

Key regulatory milestones driving the sector toward 2040

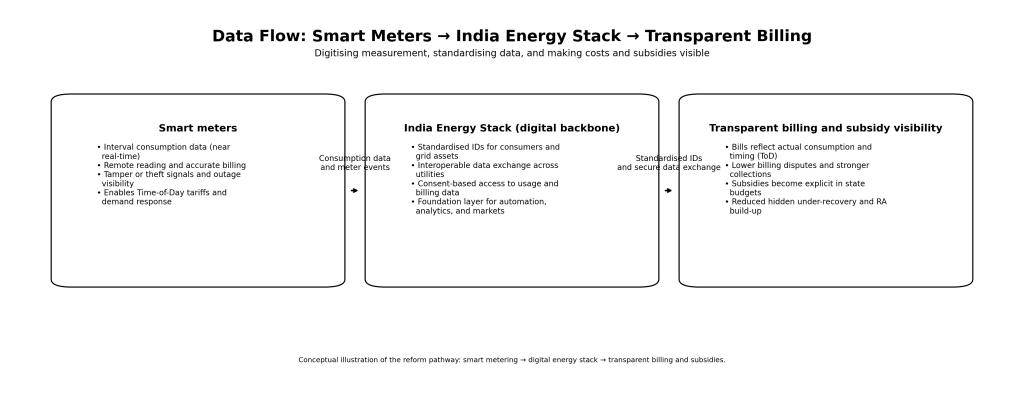

2. Technology & Digital Innovation

The smart meter rollout is, at the same time, the sector’s biggest headache and its biggest opening for change. Only ~8% of the target has been achieved, yet the benefits are undeniable:

- Accurate, theft-proof billing.

- Data-driven tariff design.

- Consumer empowerment via real-time usage data.

- Foundation for Time-of-Day (ToD) tariffs and demand response.

April 2025 also marked the launch of the India Energy Stack, a digital backbone that will link consumers, utilities, and assets. Think of it as Aadhaar for energy, an infrastructure layer that standardizes IDs and data. Once combined with smart meters, it could depoliticize tariffs. When costs and consumption are transparent in real-time, subsidies can no longer be hidden in DISCOM accounts rather they must appear in state budgets.

This is a potential game-changer: data becomes the disinfectant that forces financial discipline.

Digital transparency: shifting the burden from DISCOMs to state budgets

3. Private Participation & Market Evolution

Delhi’s privatization story is legendary. Losses cut from over 50% to under 15% in a decade. Odisha followed a similar path. But the politics remain raw.

In Uttar Pradesh, power workers kicked off massive protests in 2025 over privatization pushes, with unions sounding alarms about job cuts and the end of subsidies. States are stuck in a tough spot: privatization brings efficiency but sparks serious political blowback.

One possible middle path: partial privatization. Allow private firms to take over the most loss-making zones first, proving efficiency gains before scaling up. This hybrid approach could break the stalemate.

IV. Unlocking the Next Phase of Growth

The next 15 years hold enormous potential if reforms stick.

Renewable Growth

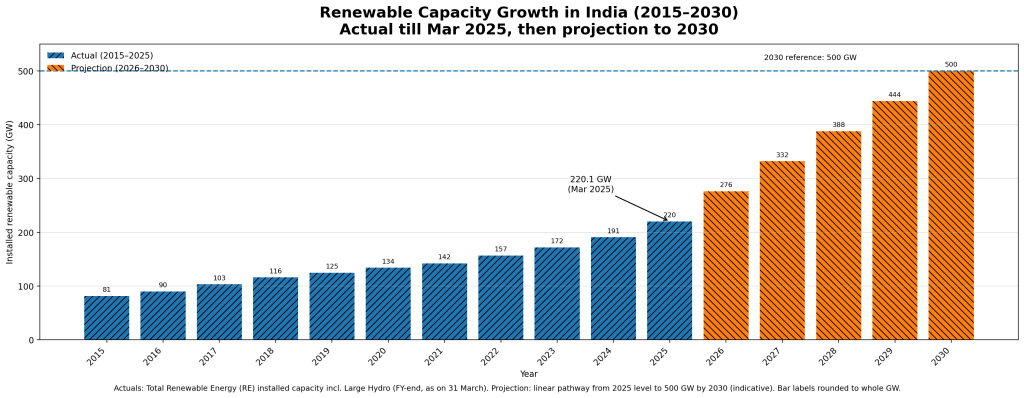

India added 28.7 GW of new renewable capacity in FY2025 , a 55% jump over the previous year. With a pipeline of 145 GW, DISCOMs have a chance to evolve into active grid managers of decentralized, variable energy.

Energy Storage

Battery energy storage systems (BESS) are ready to take off big time. India could need around 50 GW of storage by 2030 to keep the grid steady, and with battery prices dropping fast plus viability gap funding kicking in, it's turning into a massive investment playground.

Investment Wave

The sector's primed to pull in a whopping ₹40 lakh crore over the next decade, with chances exploding in smart grids, EV charging setups, and rooftop solar.

Consumer Empowerment

Smart meters + ToD tariffs = active consumer participation. Add rooftop solar schemes like PM Surya Ghar and farmer-centric programs like PM-KUSUM, and citizens shift from passive bill-payers to prosumers.

India’s renewables momentum: accelerating faster than ever before

V. Risks That Could Derail Progress

Of course, the path is not risk-free.

Policy Inertia

Smart meter rollouts remain glacial. Without speed, the data-driven reforms may stall.

Grid Instability

More renewables = less synchronous inertia. Without storage or synthetic inertia, grid stability is at risk.

Cross-Subsidy Erosion

High-paying industries are leaving DISCOMs via Green Open Access (18.7 GW cumulative capacity by FY2024, growing at 46% CAGR). This leaves DISCOMs increasingly dependent on lower-paying consumers.

The solution isn’t blocking open access, but redesigning subsidies to be transparent and targeted.

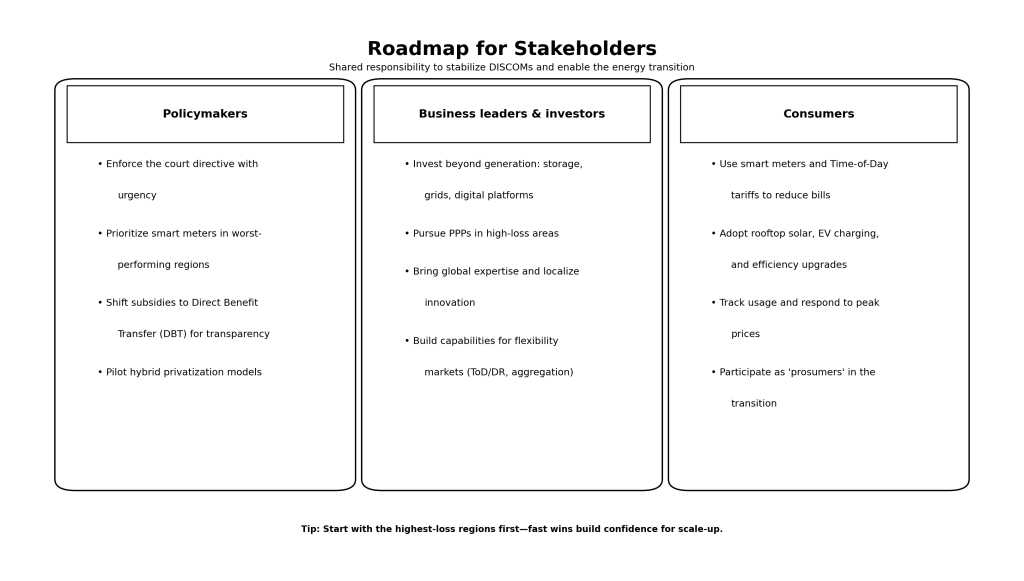

VI. A Roadmap for Stakeholders

Policymakers

- Enforce the court directive with urgency.

- Prioritize smart meters in the worst-performing regions.

- Shift subsidies to Direct Benefit Transfer (DBT) for transparency.

- Pilot hybrid privatization models.

Business Leaders & Investors

- Focus investment beyond generation: storage, grids, digital platforms.

- Pursue PPPs in high-loss areas.

- Leverage global expertise to localize innovation.

Consumers

- Use smart meters and ToD tariffs to save energy and cost.

- Invest in rooftop solar, EV charging, and efficiency upgrades.

- Recognize your role as active participants in the transition.

Reform requires shared responsibility across all stakeholders

VII. Conclusion: The Time to Act

India's power distribution sector is hitting a turning point right now. The Supreme Court's ruling has opened up a rare shot at real reform, digital tools are bringing the kind of transparency we've never seen, and renewables are charging ahead full steam. But it'll all come down to nailing the execution , without some gutsy political moves and everyone pulling together, we'll just loop back to the same old mess of delays and debt.

The next 15 years will show if DISCOMs stay a drag on everything or finally become the powerhouse driving India's green, thriving tomorrow.

Futuristic grid illustration with renewables, storage, and digital overlays