Introduction: A Financial Revolution in Motion

There’s something quietly radical happening in India’s financial corridors right now. Not in the grand rhetoric of the Union Budget, but in the quieter corners of banks, funds, and policy desks where numbers tell a more restless story. The government’s latest push — a marriage of rooftop solar dreams and nuclear partnerships — isn’t just about energy. It’s about rewriting how India moves money toward its future.

The real action? It’s not in the Parliament. It’s in boardrooms, bond markets, and the subtle re-wiring of risk appetites. The second tranche of India’s Sovereign Green Bonds (SGrBs) — slated for auction this February — isn’t merely another fiscal event; it’s a credibility test. Can India prove it’s ready for prime time in the global climate-finance arena?

The first issue earlier this year was oversubscribed, a rare sign that investors see something real here — that India’s green promises aren’t just slogans but assets worth betting on. The stakes couldn’t be higher: a trillion-dollar gap yawning between ambition and financing. Green finance isn’t a pet project anymore; it’s the bloodstream of India’s economic reinvention.

India’s clean-energy transition is as much about capital as it is about carbon

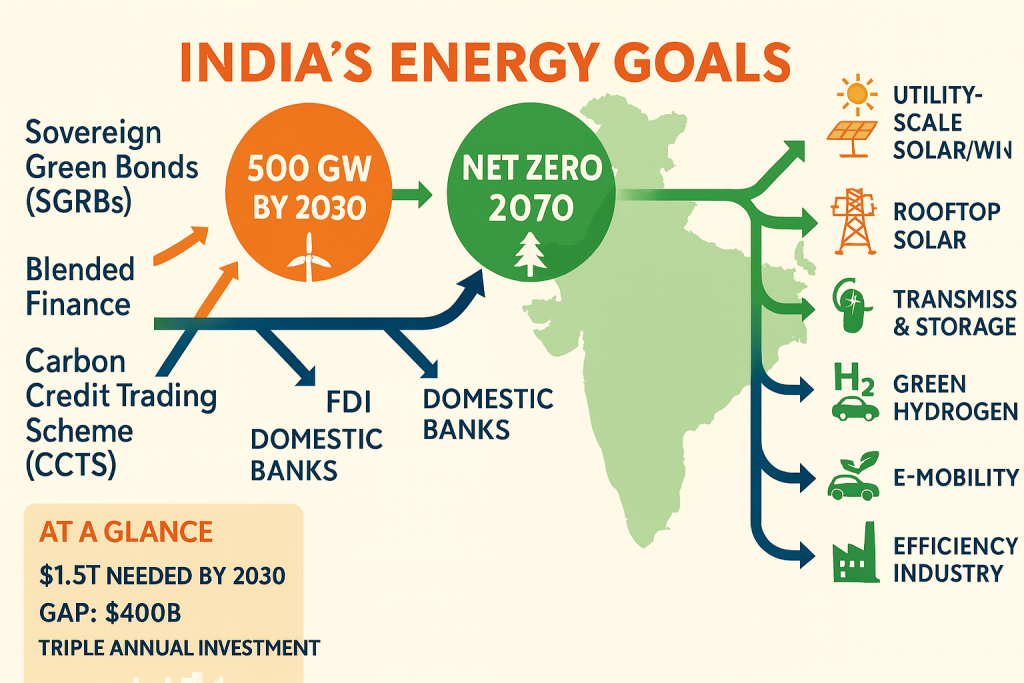

The Scale of the Challenge: Financing a Trillion-Dollar Transition

Let’s not sugar-coat it. India’s targets are breath taking — and brutal.

500 GW of non-fossil capacity by 2030. Net zero by 2070.

Those aren’t numbers on a slide deck; they’re mile-high commitments with billion-dollar price tags.

To hit them, the country needs around US $1.5 trillion in clean-energy investment by 2030. As of early 2024, we’re still about US $400 billion short. And that gap isn’t just financial — it’s psychological. Investors still whisper the same old doubts: policy flip-flops, fragile state finances, opaque regulations.

The pain points? They’re no secret:

- Policy unpredictability that keeps lenders on edge.

- Power distribution companies (DISCOMs) that can’t pay their bills on time.

- A financial system that still thinks “green” means “CSR.”

- A bond market too shallow to soak up the capital we need.

Bridging that mess will take more than good intentions; it’ll take what the pros call “financial plumbing.” In plain terms — the pipes, valves, and filters that move money safely from investors to sustainable projects without leaking trust along the way.

The Rise of Green Instruments: Building the Financial Toolkit

Here’s where India’s ingenuity starts to shine. Piece by piece, the country is building a green-finance toolkit that’s more sophisticated than many realise.

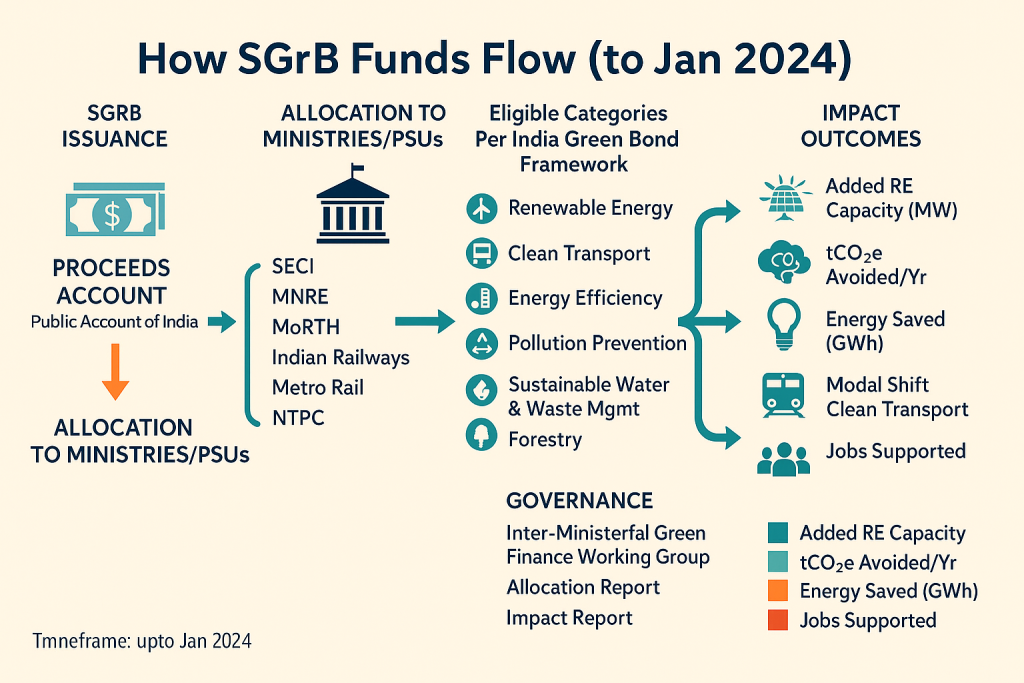

1. Sovereign Green Bonds: The New Benchmark

Those first two tranches of SGrBs, floated in January and February 2024, mark a quiet turning point. For the first time, the Indian government is using debt to fund projects with measurable environmental outcomes — solar parks, clean-transport corridors, afforestation drives.

More than the money, it’s the signal that matters. When the government backs its climate policy with fiscal muscle, markets listen. A functioning sovereign green-bond curve could soon give corporates, cities, and PSUs the pricing confidence to issue their own. It’s policy credibility, written in yield spreads.

Sovereign Green Bonds signal credibility and crowd in private capital

2. Blended Finance: Making Risk Tolerable

Next comes the India Green Finance Facility (IGFF) — still taking shape, but already promising. Partnered with the Green Climate Fund and the Asian Development Bank, IGFF aims to do something deceptively simple: make risky green sectors less scary.

Think of it as financial shock absorption. Public concessional funds take the first hit, allowing private investors to breathe easier. Green hydrogen, waste-to-energy, storage — all suddenly look bankable when early losses are cushioned. It’s not charity; it’s strategy.

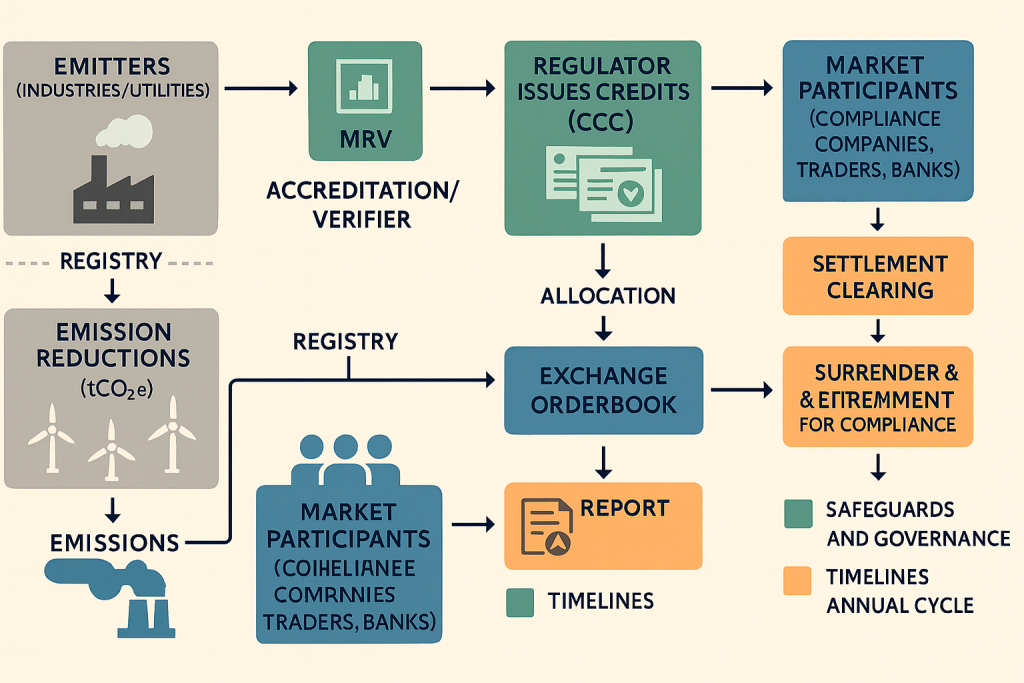

3. Carbon Credit Trading Scheme: Turning Emissions into Assets

Then there’s the upcoming Carbon Credit Trading Scheme (CCTS) — perhaps the most transformative of them all. For years, carbon was just a line in a sustainability report. Soon, it’ll be a tradable commodity.

The system starts with nine industrial sectors, focusing on emission intensity instead of raw energy use — a clever improvement on the old PAT model. Companies that outperform their benchmarks will earn Carbon Credit Certificates (CCCs) they can sell or bank. Imagine that: a market where cleaner operations translate into actual revenue.

If this takes off — and it likely will — India could host one of Asia’s most dynamic compliance carbon markets. Transparent, investable, and brutally real.

4. Sustainability-Linked Loans & Corporate Green Bonds

Meanwhile, corporate India isn’t waiting around. From Adani Green to REC Limited to Piramal Finance, firms are issuing instruments that tie financial terms to sustainability results. Miss your ESG targets? Pay higher interest. Exceed them? Enjoy cheaper credit.

It’s the first time financial discipline has truly met environmental ambition. And once that link hardens, sustainability stops being a PR line and starts being a profit lever.

Corporate India’s Response: From Compliance to Strategy

There was a time when “going green” sat in the HR or CSR section of the annual report. Those days are gone. Today, CFOs are the new climate warriors. Access to cheaper, longer-tenor finance increasingly hinges on ESG credibility.

We’re seeing this across boardrooms:

- Steel makers experimenting with hydrogen furnaces.

- Oil refiners investing in carbon-capture tech.

- Cement majors cutting clinker content like it’s cholesterol.

It’s not moral pressure; it’s economic evolution. The energy transition is no longer optional. It’s the new business model.

And here’s the twist — investors love it. Sovereign funds, climate-conscious banks, even pension funds — they’re all watching, and they’re willing to pay for good governance and green ambition.

Investor Sentiment: Confident but Cautious

Global capital has noticed India’s transformation. Over US $12 billion in FDI has already flowed into renewables. Big names are queuing up: the IFC plans to double annual financing to US $10 billion by 2030; the ADB is quietly building a clean-energy pipeline.

But let’s be honest — optimism has boundaries. Investors are no longer dazzled by glossy PowerPoints. They want predictability: stable policy on open access, clean payment mechanisms through DISCOM reform, and transparent impact data.

The message couldn’t be clearer: capital follows credibility.

The New Investor Lens

Investors now evaluate not only returns but also policy credibility and execution stability. They are demanding:

- Predictable regulations on open access and net metering.

- Reliable payment mechanisms through DISCOM reforms.

- Transparent impact reporting.

The message is clear — global capital is available, but only for credible, de-risked projects.

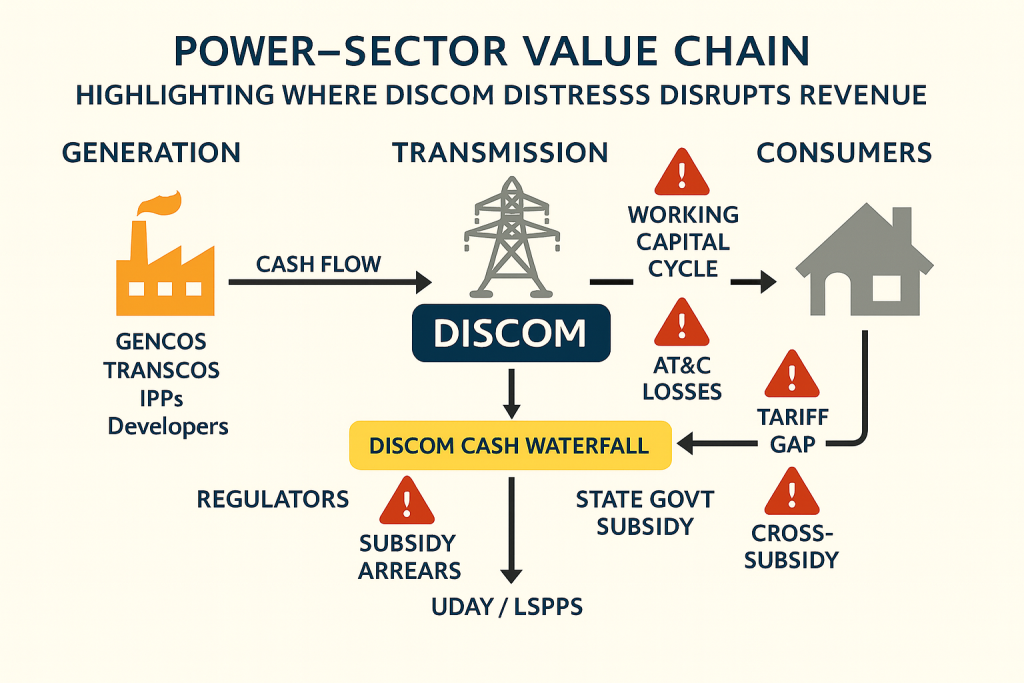

The DISCOM Dilemma: The Hidden Fault Line

India’s clean-energy ambitions rest on a wobbly foundation. Power distribution companies, or DISCOMs, are drowning in ₹6.7 lakh crore of debt. When they delay payments to renewable developers, the whole chain suffers — projects stall, lenders panic, and the market loses faith.

Until DISCOMs are reformed — through tariff rationalisation, direct subsidy transfers, digital billing, and strict accountability — no amount of fancy green bonds will plug the leak. It’s the same old story: shiny new pipes, but the joints still leak.

Financial stress at the distribution level can derail upstream investments

Households at the Heart: The Rooftop Revolution

While institutional finance grabs headlines, the real human story is unfolding on rooftops. The government’s PM Surya Ghar Muft Bijli Yojana, launched this month, aims to install rooftop solar systems for one crore households.

Subsidies cover up to 40 percent of system cost, enabling families to cut bills and earn revenue by selling surplus power back to the grid.

Yet success depends on ground realities — vendor reliability, timely subsidy disbursement, and user awareness. Without proper support ecosystems, the promise of “free power” could turn into frustration.

This program is more than an energy policy; it’s a financial inclusion story. Empowering households to become energy producers creates a distributed, citizen-driven form of green finance.

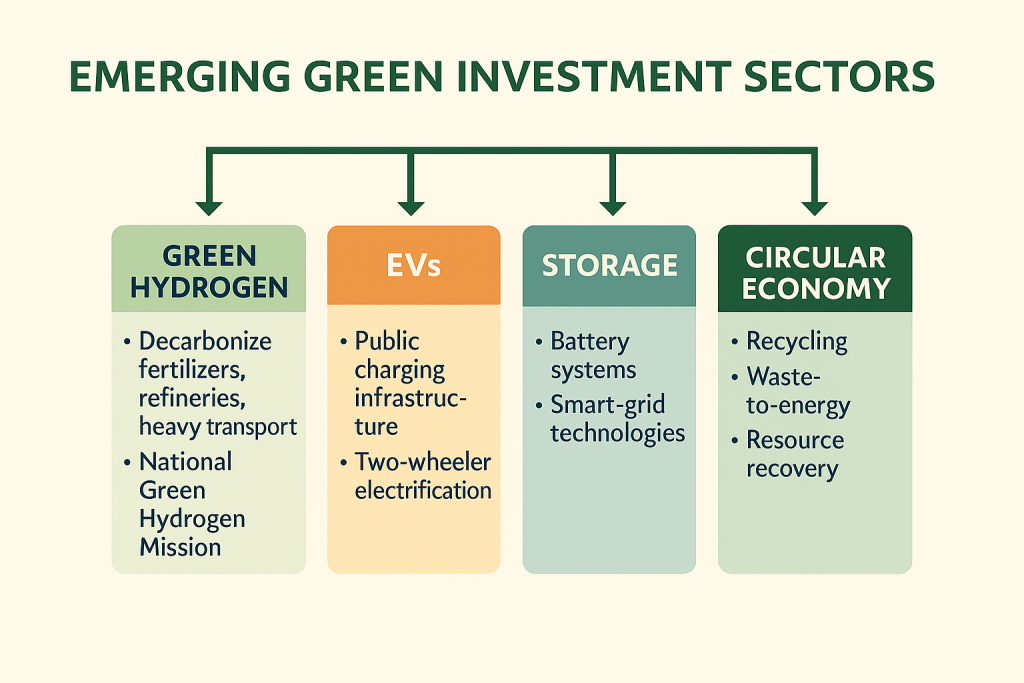

Opportunities on the Horizon

If you’re wondering where the next big wave of green investment will break, look no further:

- Green Hydrogen: nearly ₹8 lakh crore in potential investment by 2030, key to decarbonising steel, fertiliser, and heavy transport.

- Energy Storage & Smart Grids: essential to keep renewables reliable.

- Electric Mobility: the lease-to-own and energy-as-a-service models are quietly rewriting how India moves.

- Circular Economy: financing recycling, waste-to-energy, and resource recovery — the invisible half of sustainability.

Each of these sectors tells the same story: innovation meeting capital halfway.

The next growth wave extends beyond renewables to whole-economy transformation

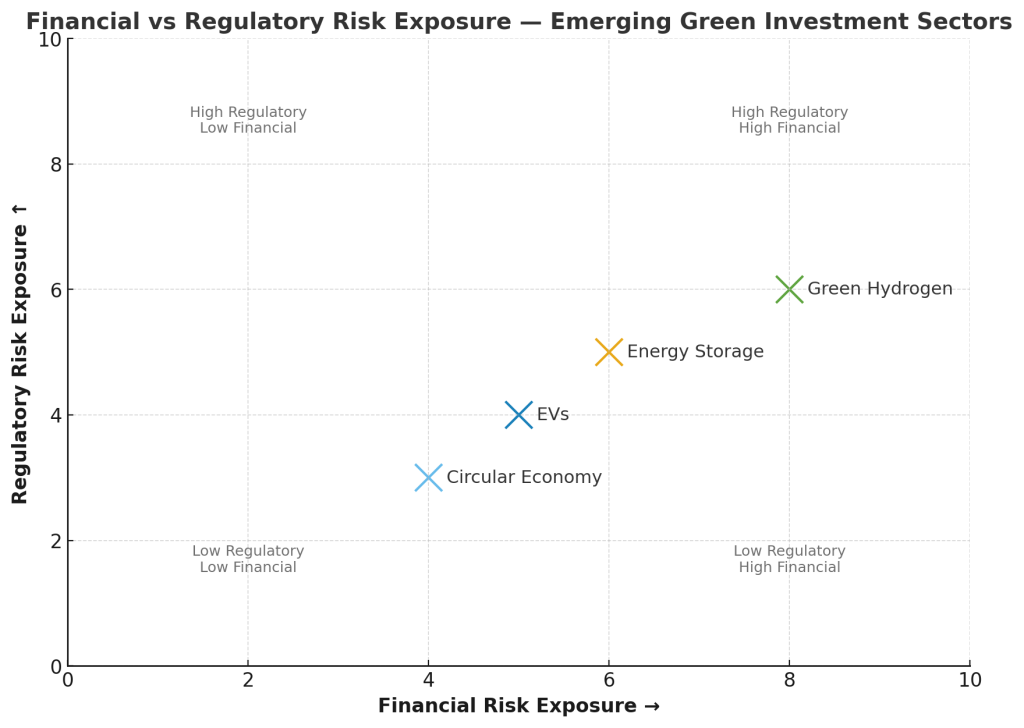

Risks That Still Loom

For all the momentum, the cracks are visible like

- Regulatory disintegration: Dissimilar state policies on net metering and open access.

- Land and grid bottlenecks: Slow approvals delay project execution.

- Limited project pipelines: Many investors cite lack of bankable projects.

- Social transition gaps: Communities dependent on fossil industries need alternative livelihoods.

As a result, some investors now demand higher yields for “green” bonds — a phenomenon dubbed the “disappearing greenium.” This reflects a maturing market where climate labels alone no longer guarantee lower borrowing costs.

Two-axis chart mapping “Financial vs Regulatory Risk Exposure

Strategic Priorities: Where the Focus Must Fall

For Policymakers:

Fix the DISCOM mess, unify green-finance taxonomies, and create a Just Transition Fund for coal-dependent states. Without that social buffer, the shift will be politically brittle.

Conclusion: Financing the Future Together

India’s clean-energy journey is no longer a dream whispered in policy circles — it’s happening, right now, in every bond issue, every rooftop panel, every new industrial pilot. Financial innovation has become our climate engine.

Between sovereign green bonds, blended-finance frameworks, and the forthcoming carbon market, India is constructing the scaffolding of an economy that rewards responsibility and scales sustainability.

But make no mistake — this is a marathon, not a sprint. Until the pipes of our financial system stop leaking — until DISCOMs pay on time and state policies stop colliding — capital will always cost more than it should.

Still, there’s reason for faith. Few nations have managed to blend scale, democracy, and ambition like India. If we hold the line — tightening the bolts on credibility and inclusion — we won’t just meet our climate goals. We’ll rewrite the global rulebook on how a developing economy funds its own future.

If these foundations hold, India will not just meet its climate targets; it will redefine how a developing nation finances growth responsibly, equitably, and at scale.