The Turning Point for India’s Offshore Ambition

Every once in a while, a policy announcement lands not as a quiet note in a government bulletin but as a strategic signal - a pivot that tells industries, investors, and engineers: “the game has changed.”

That’s exactly what happened on August 17, when the Ministry of New and Renewable Energy (MNRE) unveiled its revised offshore wind strategy. For years, India’s offshore wind potential has lived in PowerPoint slides and feasibility reports. Today, with this policy, it begins its journey into steel, concrete, and spinning blades at sea.

This isn’t just another clean energy announcement. Offshore wind represents a chance to unlock 70 GW of power potential, reshape India’s industrial base, and pair green electricity with emerging sectors like hydrogen. For technical and policy professionals, the takeaway is clear: we are at the threshold of a sector that could rival solar in strategic importance.

Why Offshore, Why Now?

India has already staked its place among the world’s renewable leaders:

- Fourth in wind power capacity.

- Fifth in solar power capacity.

- A 500 GW non-fossil fuel target by 2030 that is shaping investment flows, regulatory design, and grid planning.

But here’s the challenge: land. Onshore wind has delivered solid results, but new large sites are becoming harder to secure. Solar still has runway, but its land intensity and time-bound generation profile leave gaps.

Offshore wind addresses both problems:

- Reliability advantage: With a 40–45% capacity utilization factor (CUF), offshore wind generates more consistently than onshore wind (30–35%) or solar (20–25%).

- Grid balancing: Solar peaks mid-day and drops off in the evening. Offshore wind fills in the gaps, stabilizing supply when thermal power currently bears the load.

- Scale of resource: India’s 7,600 km coastline hides some of the most promising wind corridors in Asia, especially off Gujarat and Tamil Nadu.

For energy-hungry industries - think steel, cement, data centers - offshore wind isn’t just an alternative, it’s a lifeline for meeting sustainability targets without compromising reliability.

Breaking Down the Policy Blueprint

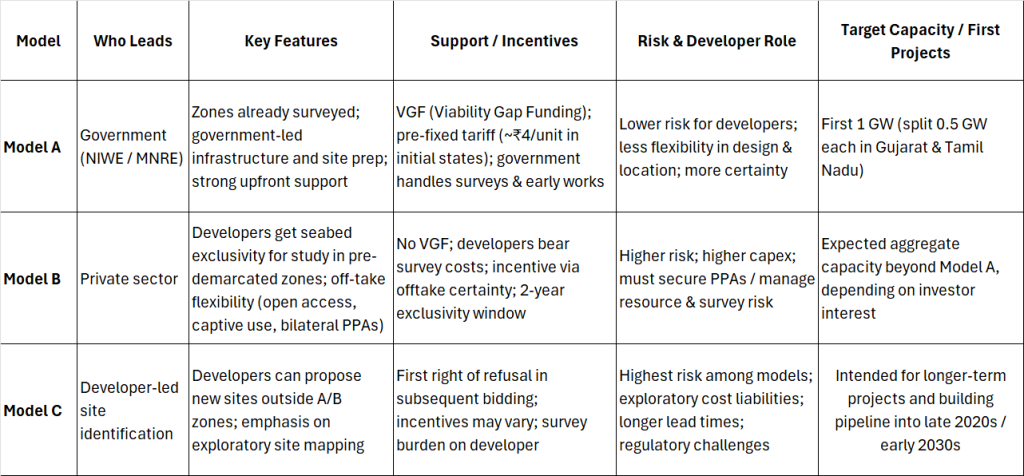

The MNRE policy sets a three-track framework designed to balance government support with private innovation:

Model A: Government-Led (VGF Support)

- The government, through NIWE, conducts resource surveys and preps sites.

- Viability Gap Funding (VGF) bridges the high initial costs.

- First tranche: 1 GW (0.5 GW each in Gujarat and Tamil Nadu) with tariffs pre-fixed at ₹4/unit.

- Aim: Give developers certainty and de-risk the first movers.

Model B: Private-Led (No VGF)

- Developers get 2-year seabed exclusivity to survey and plan.

- Energy can be sold through open access, captive models, or bilateral PPAs.

- Targets corporates with strong ESG mandates who want to “lock in” clean power for the long term.

Model C: Exploratory Path

- Developers may propose new sites beyond government-prepared zones.

- The one who does the initial groundwork gets first right of refusal in bidding.

- Encourages exploration and builds a pipeline of projects for the 2030s.

This structure is not just a set of models. It’s a signal to investors: India is serious about scaling offshore wind, but it’s doing so with diversified entry points to accommodate varying risk appetites.

Three models, one vision - how India plans to nurture offshore wind growth

DISCOMs and the Policy Puzzle

India, as one of the fastest-growing economies in the world, is experiencing a rapid rise in electricity consumption. This surge is fuelled by industrial growth, urbanization, rising incomes, population expansion, and the increasing reliance on technology and digital services.

Households are consuming more energy for appliances, cooling, and mobility, while industries and commercial sectors are demanding greater power to sustain their growth. However, this sharp increase in demand also raises concerns about greenhouse gas (GHG) emissions, given India’s historical dependence on fossil fuels for electricity generation. To address this challenge, accelerating the adoption of renewable energy sources such as solar, wind, and hydropower is not just an environmental imperative but also an economic necessity. Expanding clean energy capacity can help India meet its rising power needs while reducing carbon emissions, enhancing energy security, and moving the nation closer to its long-term climate commitments

Any renewable policy in India must consider one crucial stakeholder: DISCOMs. Their financial stress is no secret - late payments, mounting dues, and limited appetite for long-term PPAs.

Offshore wind, with its higher costs, could have been a non-starter without DISCOM buy-in. That’s why the policy’s ₹4/unit tariff agreement in Gujarat and Tamil Nadu is pivotal. It offers:

- Predictability for DISCOMs, avoiding unmanageable cost shocks.

- Certainty for developers, ensuring offtake for their power.

- Confidence for financiers, who need assurance of stable cash flows.

For technical professionals in utilities and regulatory roles, this move is more than symbolic. It’s the mechanism that could pull offshore wind into mainstream planning.

Opportunities on the Horizon

Offshore wind’s benefits go far beyond generation capacity. It’s an industrial strategy in disguise:

- Domestic manufacturing

- India doesn’t yet produce 6–15 MW class turbines. Building this capability could birth a new high-tech sector, comparable to what solar modules and batteries have done.

- This manufacturing base could also feed global markets, positioning India as a competitive exporter.

- Job creation

- From port upgrades to vessel operations, the ecosystem spans engineers, technicians, shipbuilders, logistics managers, and R&D specialists.

- Offshore wind could employ tens of thousands directly and indirectly.

- Green hydrogen synergy

- Offshore wind’s stable output is perfect for powering electrolyzers.

- With India pushing to become a hydrogen export leader, offshore could become the backbone of hydrogen hubs along Gujarat and Tamil Nadu.

- Supply chain deepening

- Port infrastructure, specialized installation vessels, and heavy component logistics represent industries within industries that will grow with offshore wind.

The Risks & Roadblocks

The risks are real, and they can’t be sugar coated:

- High capital costs: Offshore projects cost ₹180–200 million/MW, compared to ₹60–80 million/MW for onshore.

- High tariffs: Current estimates are ₹12–14/unit, far above onshore and solar benchmarks.

- Infrastructure gaps: Ports and vessels are scarce; turbine imports are unavoidable in the short term.

- Regulatory complexity: Multiple clearances can stretch timelines to years.

- Cybersecurity: Software-defined control systems introduce new vulnerabilities.

Unless systematically addressed, these could delay projects and deter private capital.

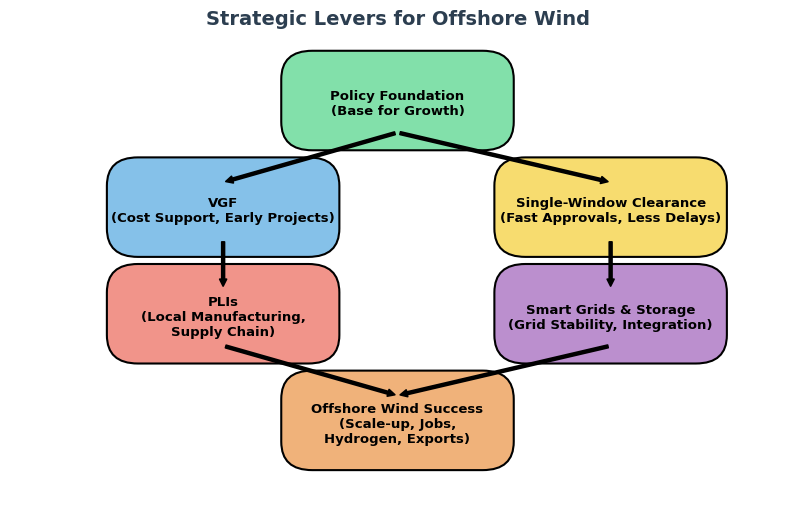

Strategic Levers for Success

.

Policy is the foundation. Execution will determine success

For offshore wind to scale, India needs to act on four levers:

- Financial Support

- Strengthen and adapt VGF.

- Explore additional tools like accelerated depreciation, green bonds, or CfDs (Contracts for Difference).

- Regulatory Streamlining

- A single-window clearance system across ministries.

- Clear timelines for approvals, modeled after best practices in Europe.

- Domestic Supply Chain

- Introduce Production-Linked Incentives (PLIs) for turbines, nacelles, and subsea cables.

- Encourage partnerships between Indian firms and global majors.

- Grid & Storage

- Offshore wind integration will require transmission corridors, smart grids, and large-scale storage.

- Long-term investments in HVDC links and battery/hydrogen storage are essential.

If these levers are pulled effectively, offshore wind could mirror the trajectory of solar: high costs at the start, rapid cost declines, and then market dominance.

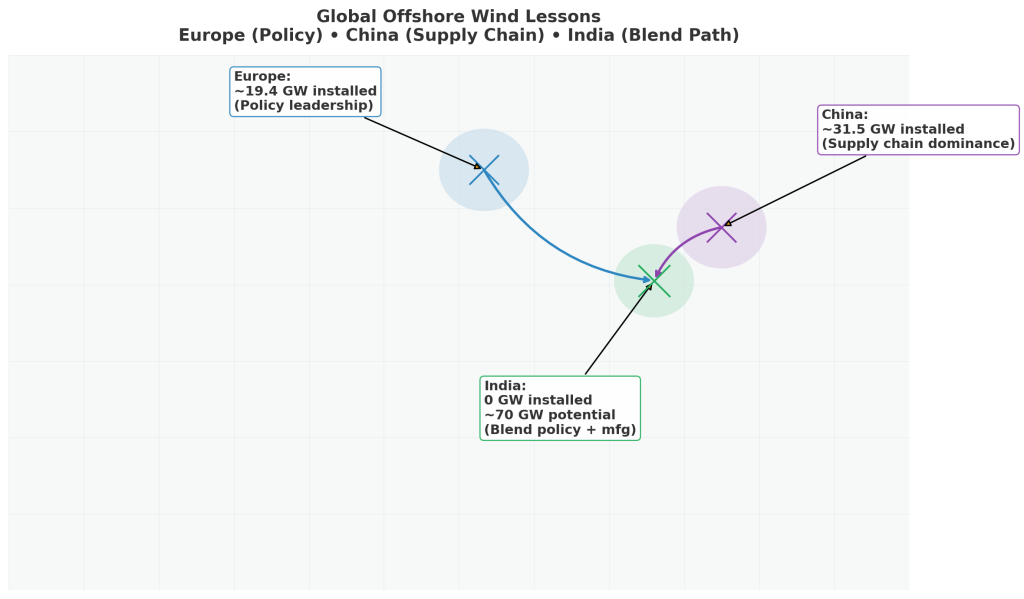

Learning from Global Leaders

- Europe’s lesson: Strong initial subsidies and predictable auctions built mature markets. Today, offshore wind competes on cost.

- China’s lesson: Building a domestic supply chain was the accelerator - from turbines to vessels, China now dominates global installations.

- India’s path: Needs a hybrid model. Import where necessary to kickstart, but aggressively build local capability for the long game.

Closing Thoughts: Anchoring a New Future

The August 2023 strategy is more than a policy - it’s a declaration of intent. It recognizes offshore wind as the next frontier of India’s energy transition.

But policies are only the foundation. The real test lies in execution:

- Will approvals be streamlined?

- Will VGF support match the scale of need?

- Can India build its own turbine supply chain before 2032?

If the answers align positively, offshore wind could not just power India’s homes and industries, but also anchor its role in global clean energy supply chains.

For policymakers, industry leaders, and technical professionals, this is the moment. Offshore wind is no longer a future scenario - it is a present opportunity waiting to be built.

India’s offshore wind policy is a foundation, not a finish line. With 70 GW potential and industrial spillovers across hydrogen, manufacturing, and jobs, it represents one of the most strategic opportunities of this decade. But the hurdles - cost, supply chain, approvals - demand coordinated execution at scale.